Selling a rental property often leads to a significant tax bill. Many landlords focus on sale proceeds but underestimate capital gains tax on BTL property, which can significantly reduce net returns.

For UK small business owners, Ltd company directors and accountants, this affects liquidity, reinvestment strategy and long-term portfolio planning.

Understanding how to avoid capital gains tax on buy-to-let property allows structured, compliant planning rather than last-minute decisions.

Key Takeaways:

Private Residence Relief, spousal transfers and allowable cost deductions are the main legal ways to reduce capital gains tax on buy-to-let property

For 2026, CGT on residential property is charged at 18% for basic rate taxpayers and 24% for higher and additional rate taxpayers

Reinvesting sale proceeds into another residential property does not defer or remove CGT liability in the UK

Capital gains tax must be reported and paid to HMRC within 60 days of completion

This article was updated and republished on 06 May 2026 to reflect current HMRC Capital Gains Tax rules, 2026 residential property CGT rates, reporting requirements within 60 days of disposal, Private Residence Relief provisions and the latest GOV.UK guidance on property disposals and compliance.

When does Capital Gains Tax apply?

CGT applies when you dispose of or sell buy to let property at a profit.

The gain is calculated as:

Sale price – purchase price – allowable costs

For 2026, the capital gains tax rate on real estate investment property remains:

- 18% for basic rate taxpayers

- 24% for higher and additional rate taxpayers

CGT must usually be reported and paid within 60 days of completion to HMRC.

Methods to reduce or avoid Capital Gains Tax on Buy-to-let property

The following are the primary lawful strategies available to UK landlords. These methods are central to understanding how to avoid capital gains tax on property, including rental and second homes.

Use Private Residence Relief (PRR)

One of the most effective answers to how to avoid capital gains tax on rental property is Private Residence Relief.

When PRR Applies:

You may claim relief if:

- The property was once your main home

- You lived in it before letting it out

You can claim:

- Relief for the period you occupied it

- The final 9 months of ownership

This reduces exposure to capital gains tax on second homes where the property previously qualified as a residence.

Temporary reoccupation before sale may qualify, but it must be genuine and not purely tax driven.

Transfer ownership to spouse

Spousal transfers are CGT-free in the UK. This strategy is frequently included in structured buy-to-let tax advice.

Benefits:

- Use two annual CGT exemptions

- Split gains across tax bands

- Reduce total capital gains on selling rental property

For jointly owned property, careful reallocation can reduce overall capital gains tax on second property exposure.

Deduct all allowable cost

Many landlords overpay because they miss legitimate deductions.

Allowable cost include:

- Stamp Duty Land Tax

- Legal and conveyancing fees

- Estate agent fees

- Survey costs

- Capital improvements (extensions, conversions, structural upgrades)

These reduce capital gains tax when selling investment property. Routine maintenance, such as repainting or minor repairs, cannot be deducted against gains. Accurate records are essential before selling a buy to let property.

Time the sale strategically

CGT depends on your total taxable income. If your income is lower in a future tax year, you may fall into the basic rate band and pay a lower rate on part of the gain.

This approach is relevant when:

- Retiring

- Reducing dividends

- Experiencing a temporary income drop

Timing is a legitimate planning method within buy to let tax strategy.

Consider a Limited Company Structure

Properties held in a company are subject to Corporation Tax on gains, currently between 19% and 25% depending on profits. This changes the treatment of capital gains tax on investment property.

Important considerations:

- No personal CGT exemption

- Dividend tax applies when extracting profits

- Transferring existing property into a company triggers CGT and SDLT

Company ownership is often discussed under searches such as landlord loopholes on how to sell your buy-to-let and pay less tax, but it is a structural decision rather than a loophole.

It requires full modelling before implementation.

Does reinvesting avoid CGT?

Yes, reinvesting proceeds into another residential property does not defer or eliminate CGT.

Unlike certain business assets, residential buy-to-let property does not qualify for automatic rollover relief. The gain remains taxable when you sell buy to let property.

Reinvestment supports portfolio growth but does not remove capital gains tax for landlords.

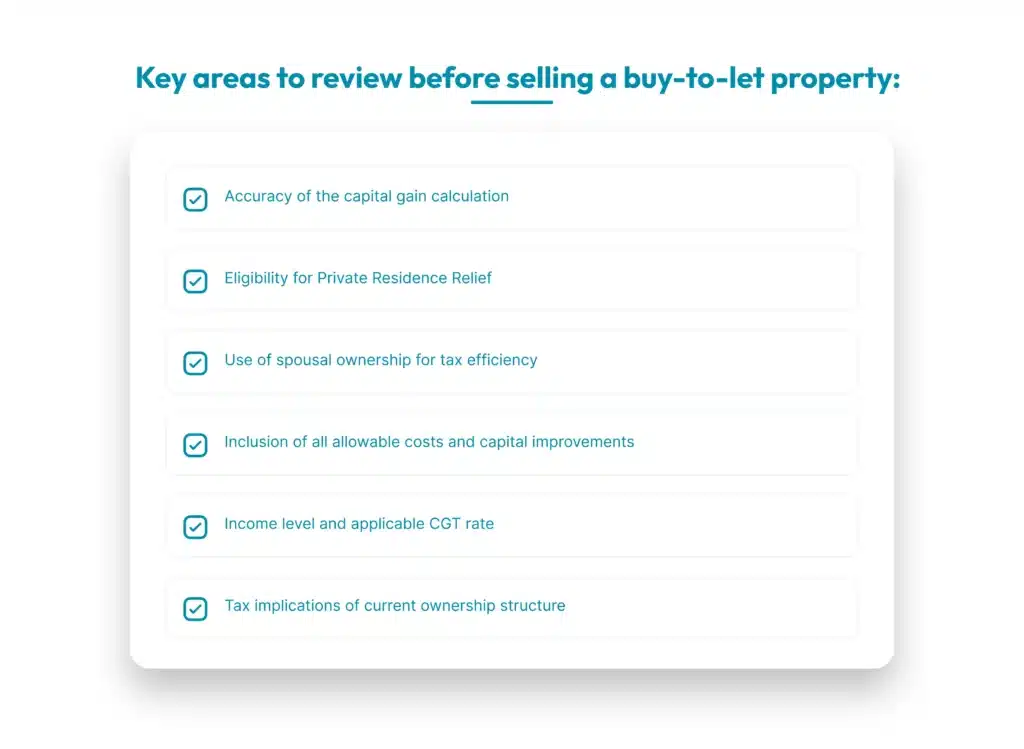

Practical CGT Reduction Checklist

Structured planning and timely buy-to-let tax advice reduce the risk of overpaying capital gains tax on BTL property.

Conclusion

Capital gains tax on a buy-to-let property can be reduced with the right steps taken before the sale. Private Residence Relief, transfers between spouses and allowable cost deductions can lower the final tax payable.

Reinvesting the proceeds does not remove the liability and holding property through a company changes how the gain is taxed rather than avoiding it.

If you are planning to sell a rental property, speak to a professional in advance to calculate the tax correctly and avoid paying more than necessary. Contact DNS CloudCo on 01908886755 or email info@dnscloudco.co.uk.

How can capital gains tax be reduced when selling a buy-to-let property?

Relief may apply if the property was once a main home. Transferring a share to a spouse and claiming all allowable costs, including legal fees and improvements, can also reduce the tax.

Does reinvesting in another property remove the tax liability?

No, buying another residential property does not delay or cancel the tax. The gain remains taxable in the year of sale.

What rate of capital gains tax applies to residential property in 2026?

The rate is 18% for basic rate taxpayers and 24% for higher and additional rate taxpayers.

Can joint ownership help lower the tax bill?

Yes, splitting ownership between spouses can use both allowances and may keep part of the gain within a lower tax band.

How soon must the tax be reported and paid after a sale?

The gain must be reported and the tax paid within 60 days of completion.

Does using a limited company remove capital gains tax?

No, a company pays Corporation Tax on gains, and further tax may apply when profits are taken out, so the liability still exists in a different form.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.