Have you paid your Class 1A NIC on time, filed your forms and still received a penalty notice from HMRC? The Class 1A NIC deadline (also known as the employer National Insurance deadline for benefits) is when most compliance issues arise.

Most employers who face this situation did not miss the deadline. They used the wrong payment reference, filed P11D without P11D(b) or reported a benefit under the wrong NIC class.

These are usually administrative errors, but once the July deadlines pass, they can create larger compliance problems. HMRC may treat the liability as unpaid even when the funds have already left the employer’s account.

This guide covers the Class 1A NIC deadlines for 2025-26, how the liability is calculated, how to pay correctly and what changes from April 2027 onward.

Key takeaways

- P11D and P11D(b) must both be filed online by 6 July 2026

- Electronic Class 1A NIC payments must clear with HMRC by 22 July 2026

- Using the wrong payment reference is one of the most common causes of HMRC payment allocation issues

- The employer NIC rate for taxable benefits is 15% for 2025-26

- Whether a benefit is treated as Class 1 or Class 1A NIC often depends on who holds the contract

- Employees can reduce certain Class 1A liabilities if they fully reimburse the benefit before 6 July 2026

- Mandatory payrolling of benefits starts from April 2027 for most employers

Class 1A NIC Deadlines for 2025-26

Class 1A National Insurance Contributions (NICs) are employer-paid charges on most taxable benefits provided to employees and directors. Employees do not pay these contributions. The employer is responsible for calculating, reporting and paying the amount due after the end of the tax year.

To stay compliant and avoid penalties, employers should make sure they are aware of the key P11D deadlines before the end of June.

| Requirement | Deadline | Method |

|---|---|---|

| P11D and P11D(b) filing | 6 July 2026 | Online only, both submitted together |

| Class 1A NIC payment | 19 July 2026 | Cheque by post |

| Class 1A NIC payment | 22 July 2026 | Electronic, cleared funds by this date |

For most employers, the key date is 22 July 2026 because HMRC must receive cleared funds by that date.

Sending payment on 22 July does not guarantee it will reach HMRC on time. Some electronic methods take up to three working days. Check your bank’s processing time before the final week of July.

6 July and the Making Good Window

Beyond the filing deadline, 6 July closes the making good window. If an employee reimburses the full value of a private benefit before this date, the Class 1A liability on that benefit is removed for 2025-26.

If reimbursement happens after 6 July, it no longer changes the 2025-26 liability. HMRC confirms this in the CWG5 2026 guidance. Company car fuel is where this most commonly applies.

Which employee benefits are subject to employer NICs?

Class 1A NIC applies to most taxable benefits in kind provided to employees and directors by reason of their employment, where the benefit is chargeable to Income Tax and not already subject to Class 1 NIC.

Common examples include:

- Company cars and fuel benefits

- Private medical insurance

- Beneficial loans

- Living accommodation

- Gym memberships and other taxable subscriptions

- Non-payrolled travel and expense benefits

- Qualifying relocation expenses above the exempt limit

How the contract determines the NIC class?

The same benefit can fall under Class 1 or Class 1A NIC depending on who holds the contract with the provider.

If the employer contracts directly with a private medical insurer for an employee, the premium is normally treated as a benefit in kind. Class 1A NIC applies and the value is usually reported on a P11D, unless the benefit is payrolled.

If the employee holds the policy personally and the employer reimburses the cost, the reimbursement is normally treated as earnings instead. In that case, Class 1 NIC applies through payroll.

The benefit itself may appear identical, but the NIC treatment, reporting method and payment process can each differ depending on how the arrangement is structured.

Which benefits are exempt from employer NICs?

The following are commonly exempt from employer NICs on benefits:

- Trivial benefits costing £50 or less, where the benefit is not a performance reward, not contractual and not cash or a cash voucher

- Benefits included in a PAYE Settlement Agreement

- Benefits used exclusively for business with no significant private use

- Employer pension contributions

For trivial benefits, the exemption only applies where the benefit:

- Is not cash or a cash voucher

- Is not contractual

- Is not linked to performance

The £50 trivial benefits exemption applies per individual benefit rather than as an annual allowance. HMRC may also consider the overall pattern and frequency of benefits provided across the tax year.

Separate Class 1A NIC rules can apply to termination awards above £30,000 and certain third-party arrangements.

How to calculate employer NIC on benefits?

Start by calculating the cash equivalent of each taxable benefit provided during the tax year. Once you have the total value, apply the Class 1A NIC rate of 15%. This gives you the total liability to report on form P11D(b) and pay to HMRC.

The cash equivalent for Class 1A purposes is the same figure reported on P11D for income tax. It is not reduced by any business use deduction the employee may claim separately.

Example:

| Benefit | Employees | Value each | Total |

|---|---|---|---|

| Private medical insurance | 8 | £1,500 | £12,000 |

| Company car benefit | 3 | £4,200 | £12,600 |

| Combined cash equivalent | £24,600 | ||

| Class 1A NIC at 15% | £3,690 |

The rate increased from 13.8% to 15% in April 2025. As a result, the same employee benefit package now creates a higher Class 1A NIC liability than it did last year. For employers with larger benefit schemes, the increase can significantly raise the July payment due to HMRC.

How to Pay Class 1A NIC to HMRC: Step-by-step process

Calculating the correct amount is only part of the process. To avoid penalties or payment allocation issues, employers must use the correct payment reference and ensure funds reach HMRC by the deadline.

Step 1: Log in to your HMRC online account

Sign in to HMRC Online Services using your Government Gateway credentials. Navigate to your employer PAYE account to confirm the total Class 1A NIC due as shown on your submitted P11D(b).

Step 2: Use the correct payment reference

Your reference is your Accounts Office reference number with 2613 appended at the end, no spaces. The digits 26 identify the 2025/26 tax year. The digits 13 identify the payment as Class 1A, not standard PAYE.

If your Accounts Office reference is 123PA00012345, the correct July 2026 reference is 123PA000123452613.

HMRC sends a pre-printed payslip with this reference each April. If it is missing, construct it from the format above or call the employer helpline on 0300 200 3200.

Step 3: Choose your payment method

- Faster Payments: Clears the same day or next working day for most banks. Best option if paying in the final days before the deadline.

- BACS: Takes three working days. Do not use this after 17 July if you want cleared funds to reach HMRC by 22 July.

- Cheque: Must reach HMRC by 19 July 2026. Post to: HMRC Direct, BX5 5BD. Allow at least three working days for delivery.

Employers paying close to the deadline generally use Faster Payments because it provides the quickest clearance.

Step 4: Allow time for funds to clear

The payment deadline is based on when HMRC receives the funds, not when the payment instruction is submitted. Processing times can vary between banks, particularly around weekends and public holidays.

For that reason, it is important to check your bank’s cut-off times and leave sufficient time for the payment to clear before the deadline. Delays of even one day can result in interest charges and late payment penalties.

P11D and P11D(b): Two Forms, Two Separate Obligations

P11D is completed for each employee or director who received taxable benefits during 2025-26. It records the benefit type and its cash equivalent value.

P11D(b) is the employer’s declaration of the total Class 1A NIC due. Without it, there is no formal record of what you owe and no payment can be correctly allocated by HMRC.

Since April 2023, both forms must be filed online only. HMRC’s April 2026 Employer Bulletin recommends submitting both forms together for 2025-26 returns to avoid incomplete return issues. Submitting one and returning to the other later is treated as an incomplete return.

If you payrolled benefits in 2025-26, P11D(b) is still required. Payrolling handles income tax collection in-year. It does not replace the obligation to declare and pay Class 1A NIC at year end.

After submission, HMRC will update your employer account to reflect the declared liability. You will not typically receive a separate confirmation letter unless there is a discrepancy.

If your online account does not reflect the submission within a few working days, contact the employer helpline to confirm receipt. That same process applies if you later discover an error in what was filed.

How to correct P11D errors after submission?

Finding an error after filing does not automatically lead to penalties. The important thing is to correct it as soon as possible.

- Amend the P11D: If a benefit has been reported incorrectly, submit an amended P11D through your payroll software or HMRC’s online service. The revised form replaces the original. An updated copy should also be provided to the employee.

- Update the P11D(b) if needed: If the correction changes the amount of Class 1A NIC due, submit a revised P11D(b). HMRC will adjust its records accordingly. Any additional amount due should be paid promptly, while overpayments may be credited or refunded.

- Contact HMRC about payment changes: Where a correction affects the amount already paid, contact HMRC to confirm the correct payment or repayment process. This can help avoid allocation issues and unnecessary delays.

Correcting mistakes early is usually far easier and less costly than dealing with them during a later HMRC compliance check.

Penalties for filing or payment failures

Before the penalties start applying, employers should understand that HMRC treats filing and payment failures separately. A return submitted on time does not prevent penalties if the payment reaches the wrong account or clears after the deadline.

Due of this, reviewing filing records, payment timing and reference details together is often just as important as calculating the Class 1A NIC liability correctly.

Late P11D(b) filing

£100 per 50 employees for each month or part-month after 19 July. If the failure continues beyond 12 months, an additional penalty up to the full value of Class 1A NIC owed may apply.

Late payment

- 5% of the unpaid amount if not cleared within 30 days of the due date

- A further 5% at six months

- A further 5% at twelve months

- Interest applies at the Bank of England base rate plus 4%. Check the current rate on HMRC’s website before calculating liabilities.

On a £10,000 liability unpaid for 40 days, the 5% penalty adds £500 and interest adds approximately £85 both accruing from the due date regardless of whether the delay was intentional.

For a small employer carrying a £25,000 benefit package, the Class 1A bill at 15% is £3,750. Left unpaid past the 30-day mark, that becomes £3,937 before interest is counted.

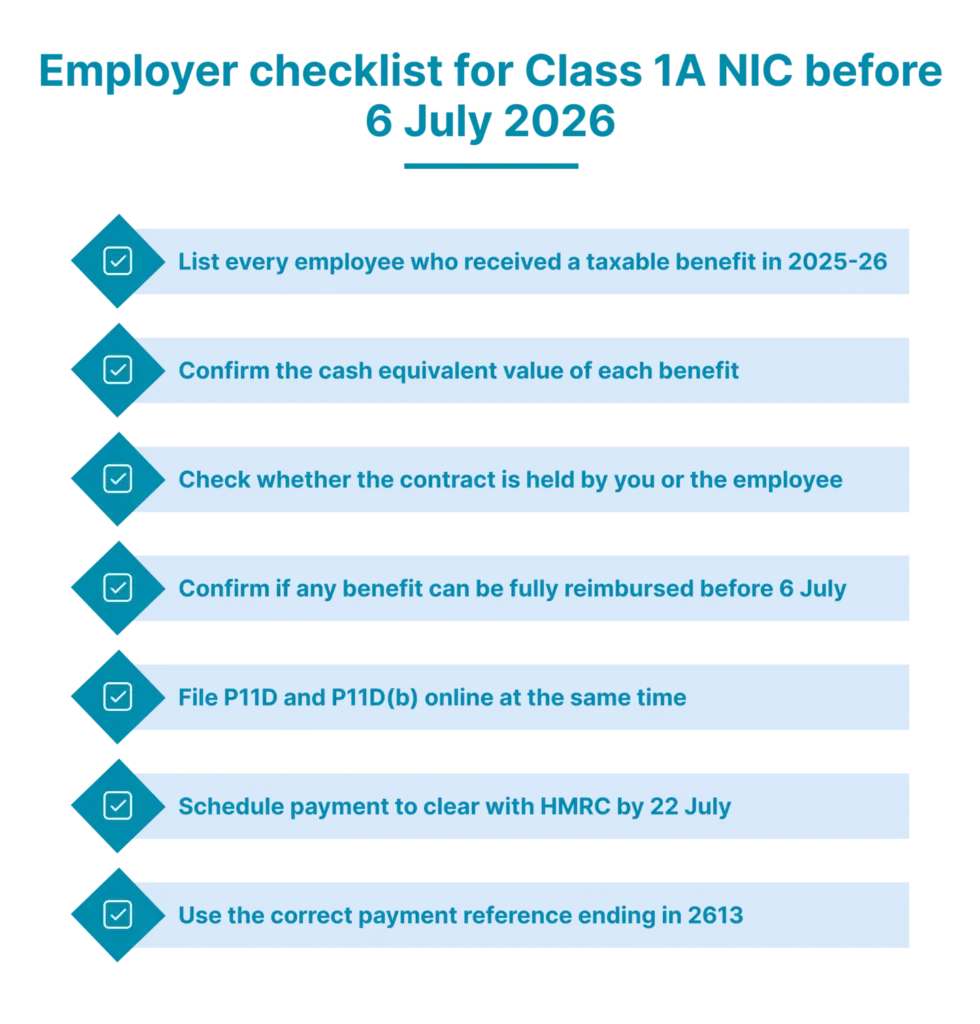

Even where filing deadlines are met, many Class 1A NIC issues arise because a key step in the process was overlooked. Reviewing benefit records, reimbursement opportunities and payment details before July can help prevent avoidable penalties and HMRC queries.

The checklist below highlights the main actions employers should complete before filing P11D returns and paying their Class 1A NIC liability for the 2025-26 tax year.

Using a structured checklist reduces the risk of missed benefits, incorrect NIC treatment and payment allocation problems.

It also helps ensure that any employee reimbursements eligible for making good are identified before the 6 July deadline.

Once these checks are complete, employers can focus on preparing for the next major change to benefit reporting. From April 2027, mandatory payrolling will significantly alter how taxable benefits and Class 1A NIC are reported and collected.

What changes from April 2027?

From April 2027, payrolling benefits in kind becomes mandatory for most employers. Class 1A NIC moves from a single annual July payment to monthly reporting and collection through payroll in real time.

The cash flow overlap

In the first year of mandatory payrolling, employers have two Class 1A obligations at once: the final P11D(b) payment for 2026-27 benefits and the new monthly Class 1A payments for 2027-28 benefits. Both fall within the same financial year.

This is subject to HMRC implementation updates and transitional guidance.

The employee impact

Employees on P11D reporting in 2026-27 will have their tax codes adjusted in 2027-28 to collect income tax owed on those benefits, at the same time as real-time deductions begin on their current year benefits.

Take-home pay can fall noticeably in April 2027 for employees with higher-value packages. Communicating this in advance avoids payroll queries that are difficult to answer at short notice.

Conclusion

Class 1A NIC compliance in July 2026 comes down to process, not just awareness of the deadline. Accurate benefit records, both forms filed together and a payment reference that reaches the right HMRC account are where most employers either get it right or do not.

This is also the last full P11D cycle before mandatory payrolling changes how Class 1A is reported and collected. Building clean records and clear ownership now reduces the administrative burden from April 2027.

Need help with P11D filing or Class 1A NIC compliance? DNS CloudCo can support with benefit reporting, calculations and HMRC submissions. Call 01908 886755, email info@dnscloudco.co.uk or visit our website for support.

FAQs

What is Class 1A NIC in the UK?

Class 1A NIC is a National Insurance charge that employers pay on most taxable employee benefits, such as company cars and private medical insurance. It is reported through a P11D(b) and paid annually.

Who pays Class 1A NIC?

Class 1A NIC is paid entirely by the employer. Employees may pay income tax on the benefit they receive, but they do not pay Class 1A NIC.

When is the Class 1A NIC payment deadline for July 2026?

Electronic payments must clear with HMRC by 22 July 2026, while cheque payments must reach HMRC by 19 July 2026.

How can employers avoid NIC penalties?

Employers can reduce the risk of penalties by filing P11D and P11D(b) forms on time, using the correct payment reference, paying by the deadline, and correcting any errors promptly.

Do I need to submit P11D(b) if I payrolled all my benefits?

Yes, payrolling handles income tax collection in-year but does not replace the P11D(b) requirement. You still need to declare your total Class 1A NIC liability and ensure payment clears by 22 July 2026.

What should employers do if Class 1A NIC was paid using the wrong reference?

Call the HMRC employer helpline on 0300 200 3200 and provide your correct Accounts Office reference and the date of payment. HMRC can reallocate a misapplied payment, but you need to act before a demand is issued and escalated. Do not send a second payment while the first is still being traced.

Does partial reimbursement before 6 July reduce the Class 1A liability?

No, HMRC requires the full value of the benefit to be made good before 6 July for the liability to be removed. A partial reimbursement before that date does not reduce the Class 1A charge proportionally. The full amount remains liable unless the employee reimburses the entire cost in time.

What happens if I file P11D forms but not P11D(b)?

The return is incomplete. Penalties on P11D(b) apply independently of whether P11D forms were filed correctly and on time.

Is private medical insurance always Class 1A NIC?

Only when you hold the contract with the insurer. If the employee holds the policy and you reimburse them, it is treated as earnings and Class 1 NIC applies through payroll instead.

What is a PAYE Settlement Agreement (PSA) and how does it relate to Class 1A?

A PSA is an agreement with HMRC where you pay the income tax on certain minor or irregular employee benefits on their behalf. Benefits covered under a PSA are not subject to Class 1A NIC. Class 1B NIC applies instead.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.