Many UK limited companies focus only on the basic fee they pay their accountant. This usually covers annual accounts, Corporation Tax returns, and routine compliance work. However, in practice, the real accounting cost for limited companies is often higher.

Extra charges arise from record corrections, late filings, regulatory queries, and additional reporting work. These are rarely discussed at the start of the engagement but can affect budgeting and cash flow.

For directors and accountants, understanding hidden accounting cost is essential. It helps businesses plan better, avoid penalties, and maintain proper compliance.

This guide explains:

- What accounting cost for limited companies really includes

- Where unexpected fees come from

- How penalties increase accounting expenses

- How to manage long-term accounting cost

Record Clean-Up and Catch-Up Work

When bookkeeping is not updated regularly, accountants must correct past records before preparing reports. This process increases accounting expenses.

Typical Charges

| Type of Work | Estimated Cost |

|---|---|

| Data clean-up | £150 to £500 |

| Error correction | £100 to £250 per hour |

| Backdated bookkeeping | £120 to £300 per hour |

This is one of the most common hidden accounting cost for limited companies in the UK.

VAT and Payroll Corrections

VAT and payroll errors increase compliance work and professional fees.

Examples include:

- Incorrect VAT rates

- Late VAT returns

- Payroll reporting mistakes

- Pension contribution errors

- PAYE reconciliation issues

Fixing these requires amended submissions and extra reviews. These services are usually charged separately. This adds to limited company accounting cost.

Companies House Penalties and Filing Charges

Late filing of statutory accounts results in automatic penalties. According to UK Government guidance, penalties include:

| Delay Period | Penalty |

|---|---|

| Up to 1 month | £150 |

| 1 to 3 months | £375 |

| 3 to 6 months | £750 |

| Over 6 months | £1,500 |

These Companies House penalties directly increase accounting expenses.

It’s important to cross-check the latest rates for any adjustments or updates to these penalties. Ensure the penalty structure is accurate for the current year.

HMRC Fines and Compliance Cost

HMRC reviews and compliance checks often require professional support.

Common situations include:

- Corporation Tax enquiries

- VAT investigations

- PAYE checks

- Expense reviews

- Director loan account reviews

Accountants usually charge separately for this work. This raises compliance cost for UK businesses.

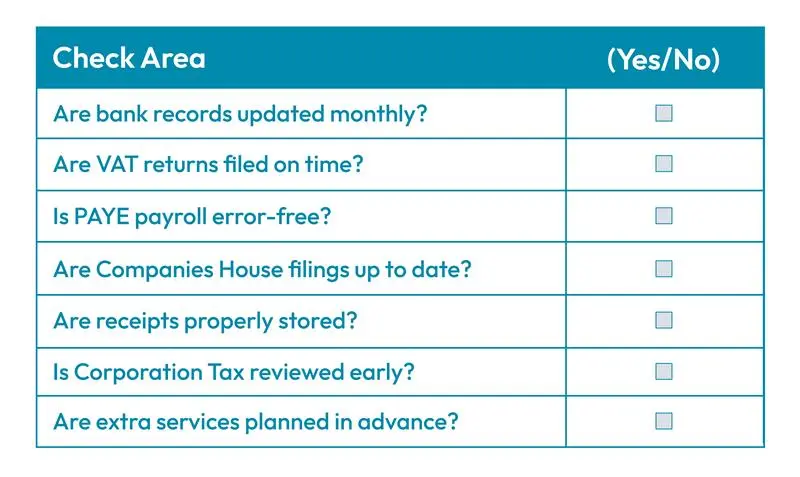

To check whether hidden accounting costs may apply, limited companies can review the following self-assessment.

Specialist Advice and Additional Reporting

As companies grow, they often need more than basic compliance.

Examples include:

- Tax planning and forecasting

- Management accounts

- Cash flow analysis

- Business restructuring support

- Profit improvement reviews

Specialist advisory services, such as tax efficiency planning or tailored financial forecasting, can significantly reduce long-term tax burdens but also contribute to increased accounting fees, particularly as the company scales.

How to Manage Compliance Costs More Effectively?

Limited companies can control hidden accounting costs by improving financial management practices.

Key steps include:

- Keeping bookkeeping updated monthly

- Reconciling bank accounts regularly

- Submitting VAT and payroll reports on time

- Maintaining organised digital records

- Reviewing accountant service scope annually

- Using cloud accounting software properly

Early preparation reduces emergency corrections, penalties, and extra billing. Proactive compliance management helps stabilise long-term accounting expenses.

Example: How Hidden Accounting Cost Builds Up

| Cost Area | Example Amount |

|---|---|

| Base annual fee | £1,200 |

| Record clean-up | £300 |

| VAT corrections | £200 |

| HMRC support | £250 |

| Filing penalty | £150 |

| Advisory work | £300 |

| Total | £2,400 |

This shows how accounting cost can increase without proper planning.

Conclusion

Hidden accounting cost for limited companies comes from record corrections, compliance work, penalties, and additional reporting requirements.

While basic accountant fees provide a starting point, the real cost of running a limited company includes much more.

With organised records, clear communication, and professional planning, directors and accountants can control these expenses and maintain strong compliance in 2026.

FAQs

It includes record clean-up, VAT corrections, HMRC compliance work, and filing penalties.

How much does an accountant cost in the UK?

Most small limited companies pay between £800 and £2,500 annually for basic services, excluding extras.

Are accounting fees tax deductible?

Yes, business-related accountancy fees are usually allowable expenses.

Why does accountant cost increase over time?

Growth in transactions, VAT registration, and reporting requirements increases workload.

How can businesses reduce unexpected fees?

By keeping records updated, meeting deadlines, and agreeing clear service scope.

Maintain monthly bookkeeping, submit returns on time, store records digitally, and review compliance requirements regularly.

What is the average cost of accountancy services for small businesses in the UK?

Small businesses typically spend between £1,000 and £3,000 per year, depending on turnover, VAT status, and service scope.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.