BR is a tax code that means 20% tax is taken from all your pay for that job or pension, with no Personal Allowance applied. But seeing it appear on your payslip for the first time is confusing. The tax deducted is higher than usual, yet nothing on the payslip explains whether that’s expected or whether something has changed.

The confusion comes from the fact that BR looks exactly the same whether it’s right or wrong. For someone with a second job, it’s often the correct code. For someone whose Personal Allowance has been assigned to the wrong income, it can quietly increase the amount of tax deducted until the issue is identified.

The important question, therefore, is not what the letters BR stand for, but why they have been applied to your income in the first place. Once that is clear, it becomes much easier to tell whether the code is working exactly as HMRC intended or whether it needs to be corrected.

Key takeaways

- Under BR, all your income from this job or pension is taxed at the basic rate, with no Personal Allowance applied to that job or pension.

- It’s usually used if you’ve got more than one job or pension.

- It’s calculated cumulatively by default, like most codes, unless HMRC separately marks it non-cumulative.

- BR is not automatically an emergency code; only codes ending in W1, M1 or X are non-cumulative emergency codes.

- If this is your only income, HMRC may not have the right details yet. Check your Personal Tax Account, update it if needed and any overpaid tax is usually refunded through your next payslip.

- HMRC’s published tax tables confirm that for code SBR you multiply the whole pay by 0.20 (20%).

What does a BR Tax Code change about your pay?

BR stands for Basic Rate and unlike most codes, it doesn’t give you any tax-free earnings before deductions start. Everything from that job or pension is taxed at 20%, starting with the first pound.

For example, if you earn £1,500 a month from a second job, the full amount is taxed at 20%, resulting in £300 being deducted. A standard tax code works differently. With an available Personal Allowance, some or even all of that income could be taxed at 0% instead.

The work you do and the amount you earn remain exactly the same. The difference comes from how the tax code treats that income.

| Standard Code (1257L) | BR Code |

|---|---|

| Personal Allowance applied: Yes (£12,570 a year) | No Personal Allowance |

| Tax rate: 0% up to the allowance, then 20% | Flat 20% on all earnings |

| £1,500 monthly earnings: Tax varies depending on available allowance | £300 tax deducted |

| Usually applied to a main job or pension | Usually applied to a second job, additional pension, or a new starter who has confirmed another current job or pension |

HMRC’s explanation of what the numbers and letters in a tax code mean confirms this is exactly how the two codes are meant to work. What it doesn’t explain is why a BR deduction can look different from one month to the next. That depends on whether the code is being calculated cumulatively or not.

Cumulative vs Non-Cumulative: How a BR Code is Calculated?

BR is normally calculated on a cumulative basis. This is confirmed by HMRC’s own PAYE Manual: PAYE11090 states that “as a rule, BR is operated on the cumulative basis.”

Each payday takes account of your pay and tax for the year so far. This keeps deductions in line with your overall position, rather than treating each pay period on its own.

Many people assume BR is always non-cumulative. That assumption is wrong for most cases.

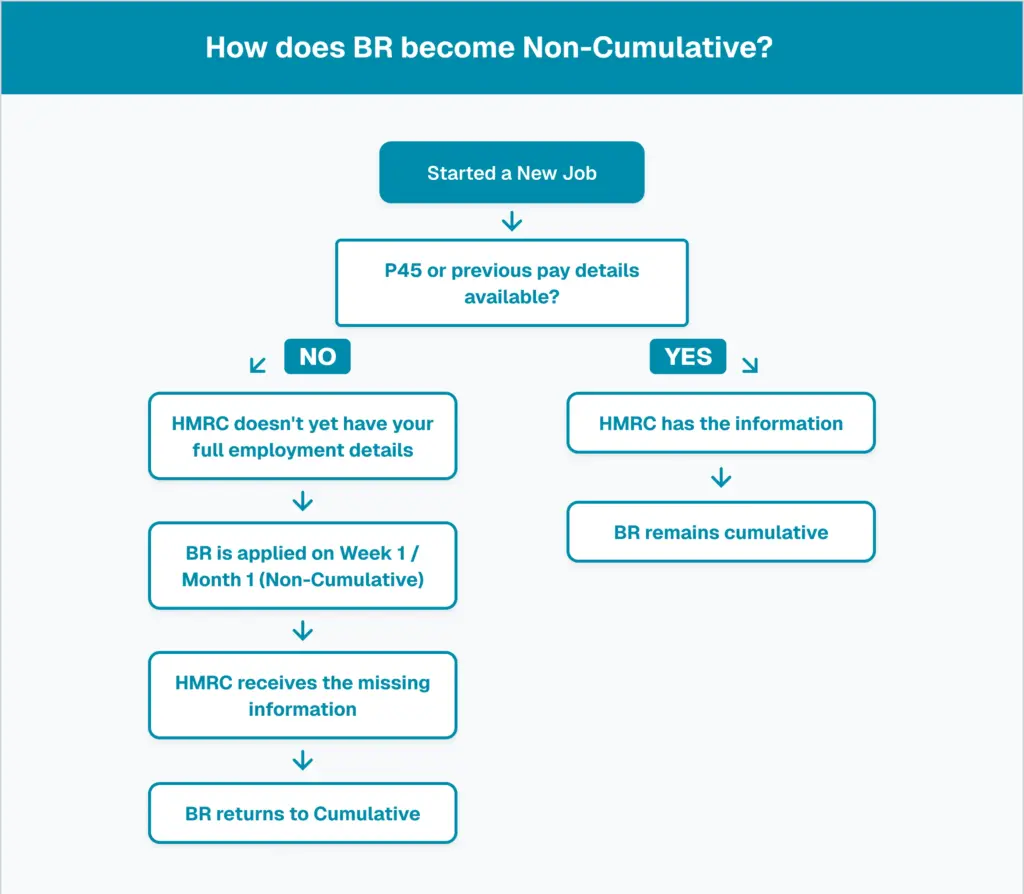

When does BR become non-cumulative?

You’re on an emergency (non-cumulative) basis if your tax code ends in W1, M1 or X (or shows NONCUM on some payslips).

This most commonly happens when someone starts a new job without a P45 or when an employer does not yet have enough information about previous pay and tax. Until HMRC receives those details, each pay period is calculated independently.

Once HMRC updates your record, employers should apply any new tax code HMRC provides as soon as possible, as explained in GOV.UK guidance on understanding employees’ tax codes.

A BR tax code is usually cumulative. It only becomes non-cumulative when HMRC or your employer does not yet have the information needed to calculate tax on a year-to-date basis.

Once HMRC receives your previous pay and tax details, the code normally returns to a cumulative basis and future PAYE calculations use your year-to-date figures.

| Basis | How it Works | Common Situation |

|---|---|---|

| Cumulative (default) | Tax is calculated using total pay and tax for the year to date. | Standard BR tax code. |

| Week 1 / Month 1 (Non-Cumulative) | Each pay period is treated separately without considering earlier pay or tax. | New starters or HMRC-directed cases. |

Don’t focus on whether the deduction changes from one payslip to the next. The more useful question is whether HMRC has all the information it needs to apply your correct tax code. Once those records are updated, the calculation usually corrects itself automatically.

The three reasons HMRC puts you on BR

Knowing how BR is calculated doesn’t explain why it’s on a particular payslip and that’s the part that actually decides whether action is needed.

You have a Second Job or an Additional Pension

This is the most common reason for a BR tax code.

Your Personal Allowance is normally allocated to one employment or pension at a time. Any additional employment or pension is often taxed using code BR, so no Personal Allowance is applied to that source.

Suppose you earn £28,000 from your main job and £4,000 from a weekend job. Your Personal Allowance is normally assigned to the main job, so the income from the second job is taxed at 20% under BR.

You started a New Job and the Starter Checklist information puts you on BR (often “Statement C”)

If you start a new job without a P45, your employer uses HMRC’s Starter Checklist to work out which tax code to operate on your first pay.

If the starter checklist shows statement C (another job or pension), the employer should use tax code BR.

Your Tax Code changed during the Tax Year

If BR appears unexpectedly after you’ve already been working for several months, it often means HMRC has updated its records.

For example, you may have started receiving a pension, changed jobs, or picked up another source of income. Any of these can mean your Personal Allowance is now being used elsewhere. Rather than assuming the code is incorrect, it’s worth checking what information HMRC currently holds before requesting a change.

In the first two situations, BR is usually the correct tax code. It’s worth checking only if the code continues after your circumstances have changed or your Personal Allowance appears to have been allocated to the wrong source of income.

BR vs Other Tax Code Letters

BR is only one of several tax codes used by HMRC. Understanding how it differs from other common codes makes it much easier to identify whether it has been applied appropriately.

| Code | Meaning | Personal Allowance |

|---|---|---|

| BR | Basic rate, 20%, applied to all pay | None |

| SBR | Scottish basic rate, 20%, applied under Scottish bands | None |

| 0T | No Personal Allowance applied, tax charged up to higher and additional rates | None |

| NT | No tax deducted at all | Not applicable |

| K | Taxable benefits or unpaid tax exceed the available Personal Allowance | Negative allowance |

BR and 0T are the two tax codes people confuse most often because neither gives a Personal Allowance. GOV.UK defines BR as all your income from this job or pension is taxed at the basic rate, and defines 0T as applying where your Personal Allowance has been used up, or you’ve started a new job and your employer does not have the details they need.

BR vs an Emergency Tax Code

Another common misconception is that BR is simply another type of emergency tax code. While both can appear when HMRC does not yet have complete information, they operate differently.

| Code | Personal Allowance | Basis | Typically applied when |

|---|---|---|---|

| BR | None | Cumulative by default | Second job, pension or new starter without a P45 |

| 1257L W1/M1 | Yes, applied per period | Emergency (non-cumulative) | You’re on an emergency code if it ends in W1, M1 or X (or shows NONCUM). |

BR removes the Personal Allowance entirely, cumulative or not. 1257L W1/M1 keeps the allowance but applies it one pay period at a time instead of against a running total. Both can cause short-term overpayment, but for different reasons and the fix for one isn’t automatically the fix for the other.

What does an SBR Tax Code mean?

If you pay Scottish Income Tax, you may see SBR instead of BR on your payslip.

Although the name is slightly different, the principle remains the same. SBR applies the Scottish basic rate of Income Tax to all earnings from that particular job or pension, without using your Personal Allowance.

SBR is commonly used when:

- Your Personal Allowance has already been allocated to another source of income.

- You have a second job or an additional pension.

- HMRC determines that this income should be taxed under the Scottish basic rate.

The main difference is where the tax rates come from. While BR follows the tax bands used across most of the UK, SBR applies the Scottish Income Tax rates for Scottish taxpayers.

Is your BR Code right for you?

Seeing a Personal Allowance disappear on a payslip is unsettling the first time it happens. In most cases, nothing has actually gone wrong. HMRC is just assuming that allowance is already being used somewhere else. The real question isn’t whether BR has appeared. It’s whether it’s attached to the right piece of income.

It is likely to be correct if:

- This is your second job.

- You receive an additional pension alongside your main income.

- Your Personal Allowance is already being used against another employment or pension.

- You have recently started a new job and HMRC is still updating your records.

It is worth checking if:

- This is your only source of income.

- Your previous employment has ended but BR is still being used.

- You believe your Personal Allowance has been assigned to the wrong employer.

- Your tax code changed unexpectedly without any obvious change to your circumstances.

If the right-hand column fits, checking a Personal Tax Account directly is worth doing rather than waiting it out. A cumulative code corrects itself once HMRC has the right information, but nothing pushes that information through on its own someone has to update it.

What does a BR Tax Code mean for Employers?

A BR tax code doesn’t only affect employees. For employers running payroll, it also means ensuring the correct tax code is applied at the right time and updated promptly when HMRC issues new instructions.

Using BR for a new starter is often the correct temporary approach when previous pay and tax information is unavailable. However, payroll responsibilities do not end there. Once HMRC receives the necessary details, employers must apply any updated tax code from the next available payroll run.

A BR code may be appropriate if:

- A new employee joins without a P45 or completed starter checklist.

- HMRC has not yet confirmed the employee’s correct tax code.

- The employee has another job where their Personal Allowance is already being used.

It may require further review if:

- HMRC has already issued a revised tax code but payroll records have not been updated.

- BR continues to be applied even though the employee’s main income is with your business.

- An employee raises concerns about consistently higher tax deductions after their circumstances have changed.

Reviewing payroll notices regularly and acting on updated coding instructions helps prevent unnecessary overpayments and avoids larger corrections later in the tax year.

Does BR affect anything beyond this payslip?

For most people, a BR tax code only changes the amount of tax deducted from their pay. However, there are a couple of situations where it can have wider implications.

If you receive Universal Credit or another means-tested benefit, your entitlement is based on the take-home pay reported through payroll. An incorrect BR code can temporarily reduce your net pay. This may affect the amount you receive, until your tax code is corrected and any overpaid tax is refunded.

If you complete a Self Assessment tax return, any tax overpaid because of a BR code is generally reconciled as part of the return. In most cases, a separate refund claim is not required.

How to Reclaim Overpaid BR Tax?

Correcting a BR tax code and reclaiming any tax you’ve already overpaid are two separate steps. Once HMRC has the correct information, the process is usually simple.

Step 1: Confirm why you’re on a BR Tax Code

Start by checking whether BR has been applied correctly. Review your latest payslip, P45, starter checklist or Personal Tax Account to confirm which job or pension your Personal Allowance is currently assigned to.

Step 2: Update your Details with HMRC

If the code is incorrect, update your employment or pension details through HMRC’s Check your Income Tax service, signing in with your Government Gateway or GOV.UK One Login details. If you cannot use the online service, you can contact HMRC’s Income Tax helpline for individuals and employees to update your records instead.

If you’ve recently started a new job, HMRC may take some weeks to process the change and issue a revised tax code.

Step 3: Check your Next Payslip

Once your employer applies the updated tax code, any tax you’ve overpaid is usually refunded automatically through payroll.

- Monthly payroll: The refund often appears in your next payslip.

- Weekly payroll: The adjustment may take slightly longer to catch up, since each weekly payslip carries a smaller share of the correction than a monthly one.

Step 4: Claim Older Overpayments if needed

If your BR tax code has been wrong for longer than the current tax year, you may still be able to reclaim overpaid tax. HMRC’s Self Assessment Claims Manual states that under SACM12155, claims must be made within 4 years after the end of the relevant tax year.

This means older overpayments are not automatically lost once the current tax year ends.

Use GOV.UK’s Claim a tax refund service to start the process. It will guide you to the right method based on your circumstances, whether that is through your Personal Tax Account, a repayment claim form or a Self Assessment return. If you believe you’ve paid too much tax under BR for several years running, review each year separately. The 4-year window is counted from the end of each individual tax year, not from when you first noticed the error.

Quick Checklist

Before contacting HMRC, make sure you have:

- Your latest payslip

- Your P45 or completed starter checklist (if applicable)

- Details of all current jobs and pensions

- Access to your Personal Tax Account

- Confirmation of which income should receive your Personal Allowance

Having this information to hand usually makes the process quicker and helps HMRC update your records more accurately.

Conclusion

A BR tax code is not necessarily an error and is commonly used for a second job, pension or new employment where HMRC has not yet applied the Personal Allowance to the correct income source. It is important to check the context of your earnings to ensure the code has been applied appropriately.

If a BR tax code appears on a main job or deductions look higher than expected, it usually means HMRC records need updating. Once corrected, PAYE is adjusted and any overpaid tax is typically refunded or balanced automatically.

For help with BR tax code issues, PAYE corrections or payroll queries, DNS CloudCo offers specialist UK accountant support. Call 01908 886755, email info@dnscloudco.co.uk or book your consultation today.

Frequently Asked Questions

Why am I on a BR tax code if I only have one job?

This usually means HMRC has incomplete information, such as a missing P45 or hasn’t yet processed the correct code. Checking a Personal Tax Account confirms whether employment details are current.

Is a BR tax code always wrong on a main job?

Not always, but it’s uncommon. If this is genuinely the only income, BR almost always means the Personal Allowance hasn’t been applied yet.

Does a BR tax code mean I’m being taxed more than everyone else?

Not more than the rate itself allows. It’s a flat 20%, the same basic rate everyone pays on standard earnings, just without the tax-free portion applied first.

How is a BR tax code different from a K tax code?

BR taxes pay at 20% with no allowance. A K code goes further, adding untaxed income, such as benefits, on top of pay before working out the deduction.

Can a BR tax code change without me doing anything?

Yes, if HMRC receives new information, such as another job ending, it can update the code automatically, usually reflected in the next payslip.

Will switching from BR to a standard code affect my next payslip amount?

Yes, usually positively. Once a code that applies the Personal Allowance replaces BR, less tax is deducted and any overpayment is typically refunded through the same payslip.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.