The second payment on account must reach HMRC by midnight on 31 July. Before making the payment, it is worth checking that the amount is correct, that a payment is actually due and that any available reduction options have been considered. Spending 10 minutes on this checklist can save you from unnecessary interest charges or overpaying tax.

This checklist covers what needs to be confirmed and actioned before 31 July: the amount owed, whether it is even required, how to pay it, whether it can be reduced, and what to do if paying in full is not possible right now.

This applies to all UK taxpayers in the Self Assessment payments on account system: self-employed individuals, partners in a partnership and company directors with untaxed income above the qualifying threshold.

Key takeaways

- The second payment on account is due by midnight on 31 July each year.

- Each instalment is normally 50% of the previous year’s Self Assessment tax bill.

- Payments on account apply only if last year’s bill was over £1,000, unless 80% or more was already paid through PAYE.

- Interest applies at 7.75% a year, charged daily at the Bank of England base rate plus 4% from 6 April 2025, and subject to change when the base rate changes.

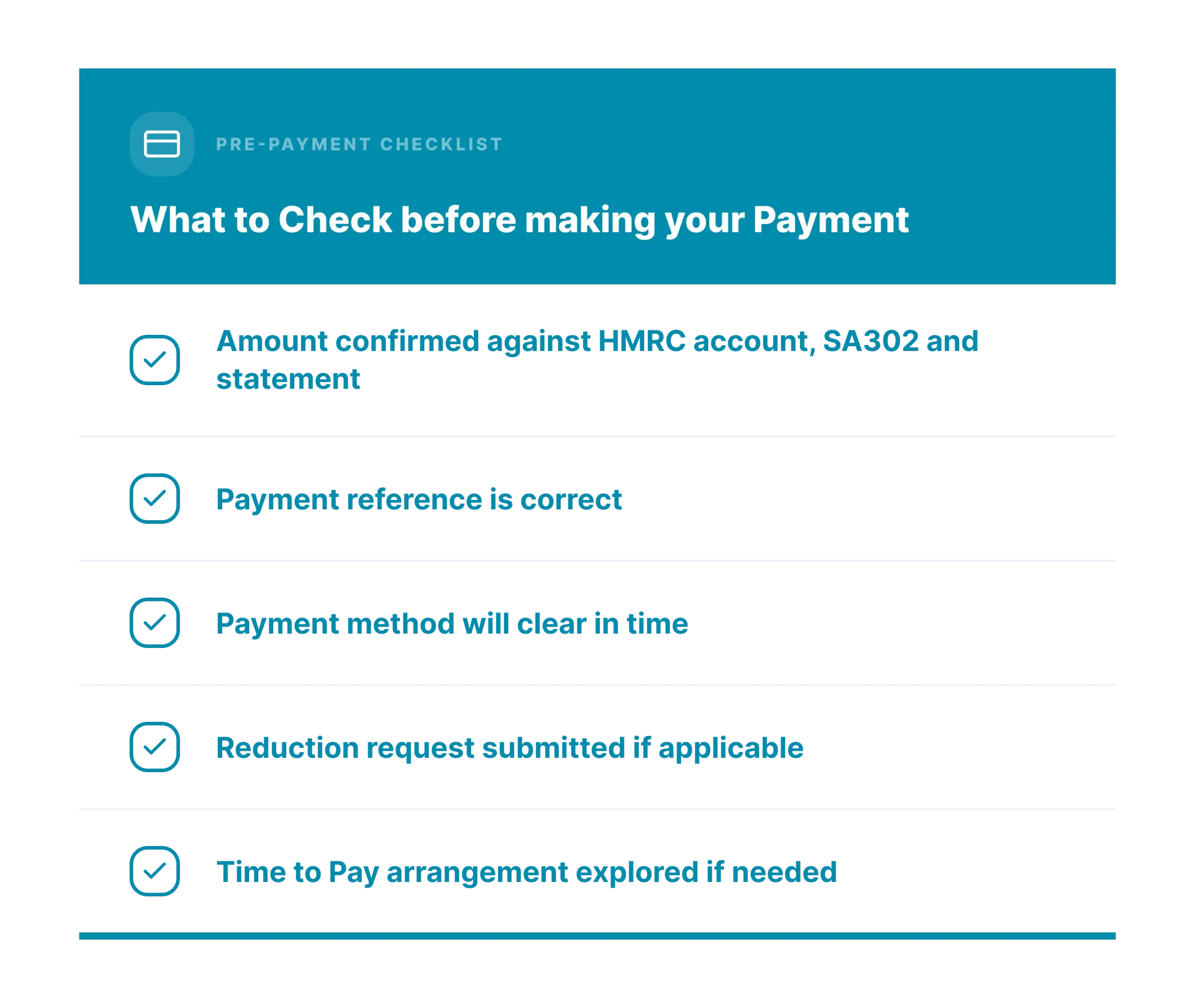

- Payments can be reduced using form SA303 if income for the current year is expected to be lower.

- A Time to Pay arrangement can be requested online if the full amount cannot be paid by 31 July.

What to review before making your Second Payment on Account?

Before paying HMRC, it is worth confirming a few details. A short review can establish that the amount is correct, that the payment is actually required, and that any available options have been considered before the 31 July deadline.

Step 1: Confirm the amount HMRC has calculated

HMRC collects Self Assessment tax in advance rather than waiting for the full amount after the tax year ends. Each payment, due on 31 January and 31 July, is normally half of the previous year’s liability, including Class 4 National Insurance if you’re self-employed.

The amount due is already calculated and visible in the HMRC online account or the most recent Self Assessment statement. Confirming the figure mainly involves checking the right documents: the SA302 tax calculation, the most recent Self Assessment statement, and the online account summary, all of which show the same figure if everything is up to date.

The calculation depends entirely on last year’s tax bill, not on current-year income.

| Previous year’s total tax bill | First payment (31 January) | Second payment (31 July) |

|---|---|---|

| £6,000 | £3,000 | £3,000 |

| £10,000 | £5,000 | £5,000 |

Because the figure is based on last year’s results, a strong previous year followed by a quieter one can produce a payment that is larger than current income supports.

Why does the July Payment sometimes feel higher than expected:

Many taxpayers remember making a large payment in January and are surprised when another payment falls due in July. January often includes both a balancing payment for the previous tax year and the first payment on account for the current year. In contrast, July only includes the second payment on account.

By comparison, July only includes the second payment on account, but the gap between payments can make it feel less expected.

Even where the amount feels higher than anticipated, it is worth checking whether the figure itself is correct before assuming an error has been made.

If the figure looks wrong:

A figure that doesn’t match expectations is usually due to one of these: a recently amended tax return, a return filed after the original calculation was issued, an HMRC adjustment that hasn’t yet appeared on the account summary, or an earlier payment that wasn’t allocated correctly.

Checking the online account against the most recent statement usually identifies which of these applies. If the reason is not immediately clear, it is worth resolving the difference before making payment, as amended returns, HMRC adjustments and payment allocation issues can all affect the amount shown.

Quick check:

Does the figure in the HMRC online account match the figure on the SA302 and the latest statement? If any of the three show a different number, the online account should be treated as the most current source.

Tip:

Checking this figure as soon as the previous year’s return is filed, rather than waiting until closer to July, gives more time to plan for it.

Even if the figure is correct, you may not need to pay in July if either condition applies. The payments on account rules only apply in specific circumstances, which makes it worth checking whether a payment is required before proceeding.

Step 2: Check whether a payment is actually required

Not every Self Assessment taxpayer owes a second payment on account, even if one was paid in January. No payment on account is required if either condition applies:

- The previous year’s tax bill was £1,000 or less.

- 80% or more of the previous year’s tax was already collected at source, for example through PAYE or interest taxed before receipt.

This is worth checking directly rather than assuming, since a £0 balance sometimes confuses taxpayers who remember paying in January and expect a repeat charge in July.

Common mistake:

Many taxpayers assume that because they paid in January, the July amount will automatically be the same. If either condition above applies, the account should show £0 for this instalment instead.

A related point worth checking: payments on account include Class 4 National Insurance for self-employed taxpayers, not just income tax. Someone estimating their own figure from memory sometimes leaves this out, which produces a number lower than what HMRC has actually calculated.

Where a July payment is due, the next consideration is whether last year’s figures still provide a fair basis for the current year’s liability. That question becomes more relevant when income has changed significantly.

Step 3: Decide whether the payment should be reduced

A reduction lowers the amount paid now, but it carries a financial cost if the estimate is wrong. The comparison below covers both sides.

| Key consideration | Reducing the payment | Not reducing the payment |

|---|---|---|

| When it applies | Current year income is reasonably expected to be lower than last year | Income is uncertain or expected to match last year |

| Benefit | Lower payment due now | No risk of an interest charge later |

| Risk | Interest charged on any shortfall if the actual bill is higher than the reduced amount | Possible overpayment, refunded or carried forward |

| How to apply | Form SA303 or HMRC online account | No action required |

Interest on an underpaid reduction is currently 7.75% a year. The rate HMRC pays on overpayments is 2.75% (effective from 9 January 2026).

An inaccurate reduction costs more than a small overpayment, which is the main factor to weigh before applying. A simple example shows when a reduction may be worth considering.

For example:

A self-employed taxpayer paid a total tax bill of £12,000 for the previous tax year, producing two payments on account of £6,000 each, due in January and July. Freelance income then fell by 40% during the current tax year.

Because the current year’s liability is likely to be lower than the previous year’s, a reduction may be appropriate, calculated on a reasonable estimate of the new figure rather than the original £6,000.

Practical tip:

Base the estimate on actual trading figures wherever possible rather than a broad assumption about the year ahead.

One issue that often emerges after a reduction request is that income can end up being higher than expected. Dividends, property disposals and additional contract work can all increase the final tax liability.

A reduction that looked reasonable in July can become too low once all income is included in the final return. Reviewing all expected income sources before submitting an SA303 can help avoid an unexpected interest charge later.

Even where the amount is correct, problems often arise because of payment timing or an incorrect reference. A payment that reaches HMRC late can still attract interest regardless of whether the calculation itself was accurate.

Step 4: Confirm your payment method and reference

HMRC accepts payment through online banking, Faster Payments, Direct Debit, debit or credit card via the GOV.UK payment page, or by cheque. Faster Payments and card payments clear the same or next day. Cheques need more processing time and carry more risk close to a deadline.

The payment must include the correct Unique Taxpayer Reference. An incorrect reference can delay HMRC allocating the payment to the account, even if the funds left the payer’s account on time.

Quick check:

Does the chosen payment method clear in time to reach HMRC by midnight on 31 July?

Step 5: Check whether a Budget Payment Plan would help going forward

A Budget Payment Plan allows weekly or monthly payments toward future tax bills instead of one lump sum each July and January.

This is separate from Time to Pay and not linked to financial hardship. It can be set up directly with HMRC and will not change the current payment, but it reduces the size of future lump-sum payments.

Tip:

This is worth setting up immediately after this payment is made, while the size of the lump sum is still fresh enough to make the case for spreading the next one.

Step 6: Consider your options if full payment is not possible

A Time to Pay arrangement allows the outstanding amount to be spread across instalments. The arrangement must be requested and is not applied automatically.

Contacting HMRC before 31 July gives more options than contacting HMRC after the payment is already overdue.

Common Mistakes to avoid in the UK (before 31 July)

A few errors come up repeatedly around this deadline:

- Assuming the July payment is based on current-year income rather than last year’s tax bill.

- Forgetting that payments on account include Class 4 National Insurance for self-employed taxpayers, not income tax alone.

- Reducing a payment without a reasonable estimate behind the new figure.

- Using an incorrect or incomplete Unique Taxpayer Reference.

- Leaving a bank transfer or cheque until the final day, when slower payment methods may not clear in time.

Before payment is submitted, below are the points worth confirming.

Practical tip:

Save a copy of the payment confirmation and the HMRC reference once payment is made. If a query arises later, having this evidence readily available avoids unnecessary follow-up.

What happens if the payment is made late?

Interest is charged daily on any amount unpaid after 31 July, starting from 1 August. The current rate is 7.75% per annum (effective from 9 January 2026), set at the Bank of England base rate plus 4%.

Interest accrues for as long as the balance remains unpaid, so the total cost increases the longer the payment stays outstanding.

You may benefit from a review before 31 July if:

- Income has fallen significantly compared to the previous year.

- Multiple income sources are involved.

- A payment reduction is being considered.

- HMRC’s calculation appears higher than expected.

- A Time to Pay arrangement may be needed.

Understanding the rules is straightforward. The uncertainty starts when you’re unsure if they apply to your specific situation.

Conclusion

The second payment on account is based on previous tax-year figures, which means the amount due does not always reflect a taxpayer’s current position. Before making payment, it is important to confirm that the calculation is correct, that a payment is required and that any available reduction options have been reviewed.

Where income has changed, the figures appear higher than expected or there is uncertainty about the amount due, additional support may help avoid unnecessary costs later.

DNS CloudCo works with self-employed individuals, directors and landlords on Self Assessment payments on account, including reviewing reduction requests and communicating with HMRC where required.

If you would like a review before the 31 July deadline, contact the team on 01908 886755 or email info@dnscloudco.co.uk. More information is available through DNS CloudCo.

FAQs

What is a second payment on account?

It is the second of two advance instalments toward the current year’s Self Assessment tax bill, due 31 July. It is calculated as 50% of the previous year’s tax liability, including Class 4 National Insurance for self-employed taxpayers.

Why does my second payment on account show as £0?

This applies if the previous year’s tax bill was £1,000 or less, or if 80% or more of the tax was already collected through PAYE or at source. In either case, no payment on account is required.

Can I pay my second payment on account early?

Yes, HMRC accepts payment any time before the 31 July deadline through the online account, Faster Payments, Direct Debit or card. Paying early removes the risk of processing delays close to the deadline.

What happens if I cannot pay my second payment on account in full?

Contact HMRC before the deadline to request a Time to Pay arrangement, which spreads the amount across instalments. Interest still applies to the outstanding balance under this arrangement.

How is the payment on account amount calculated?

HMRC takes the total Self Assessment tax bill from the previous year and splits it into two equal payments, due 31 January and 31 July. For self-employed taxpayers, Class 4 National Insurance is included in that figure.

Can landlords reduce their payment on account?

Yes, if rental income for the current year is expected to be lower than the previous year. The same SA303 process applies, based on a reasonable estimate of reduced income.

What if my income has increased this year?

No action is needed. Payments on account are based on the previous year’s figures, so HMRC will collect any shortfall as a balancing payment on 31 January. Where income has increased significantly, it may be worth setting aside the expected difference rather than waiting for the January bill.

Can I set up a Direct Debit for my second payment on account?

Yes, a single Direct Debit can be set up through the HMRC online account using the 11-character payment reference. Allow five working days for a first-time Direct Debit to process, and three working days for subsequent payments using the same bank details. For regular contributions toward future bills, a Budget Payment Plan is a separate option.

When does Making Tax Digital affect payments on account?

Making Tax Digital for Income Tax is being phased in from April 2026. The payment deadlines of 31 January and 31 July do not change under MTD, but the late penalty regime does. Taxpayers within MTD are subject to a points-based penalty system for late submissions, replacing the current 5% surcharge structure for payments on account.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.