UK payroll involves legal obligations that repeat on every payday, every month and at year-end. When one of these is missed, whether a late submission, an incorrect rate, or a missed deadline HMRC may issue a penalty.

The 2026/27 tax year has brought changes that affect payroll costs and processes for most employers, including a lower employer NIC threshold, SSP payable from the first day of absence and a new default student loan plan.

This checklist covers every payroll compliance requirement for UK businesses and employers in 2026/27 registration, rates, recurring submissions, pension obligations, record-keeping and penalties.

Key takeaways

- The Full Payment Submission (FPS) must reach HMRC on or before every payday

- PAYE and NIC payments are due by the 22nd of each month electronically (19th by post)

- National Living Wage for workers aged 21 and over is £12.71 per hour from 1 April 2026

- Statutory Sick Pay is £123.25 per week from 6 April 2026 and applies from day one of absence

- Employment Allowance is £10,500 for 2026/27 and must be claimed via EPS

Common Payroll Compliance Mistakes UK Employers make

Payroll penalties in the UK follow a pattern. The same errors appear across businesses of every size and most of them are entirely preventable.

- Missing FPS deadlines: The Full Payment Submission (FPS) must be sent to HMRC on or before payday. Late submissions can trigger monthly RTI penalties ranging from £100 to £400, depending on the size of the PAYE scheme. Using payroll software with automatic FPS submissions helps reduce the risk of missed deadlines.

- Incorrect tax codes: A wrong tax code left uncorrected accumulates underpayments or overpayments across every pay run. HMRC coding notices must be applied as soon as they are received.

- Wrong student loan plan: Applying an incorrect plan results in the wrong deduction on every pay run. The plan is confirmed through the new starter checklist and should be checked against HMRC’s student loan guidance where there is any uncertainty.

- Not updating NIC thresholds: The employer NIC secondary threshold reduced from £9,100 to £5,000 from 6 April 2025. Payroll software not updated at the start of the tax year will calculate employer NIC incorrectly on every pay run.

- Pension errors: The most common pension errors are failing to enrol an eligible employee on time, calculating contributions on the wrong earnings figure, and missing the three-year re-enrolment cycle. Each carries a separate penalty from The Pensions Regulator.

Knowing where payroll compliance breaks down makes it easier to follow the correct process. The step-by-step checklist below covers everything that needs to be in place.

What Payroll Compliance in UK requires?

Payroll compliance means meeting every obligation HMRC places on employers accurate deductions, timely submissions, correct rates and proper records. When any part of this breaks down, the consequences range from penalty points and financial charges to HMRC enforcement and public naming for NMW breaches.

The obligations below are not one-time tasks. Most recur with every pay run, every month and every tax year. The checklist that follows organises them in that order.

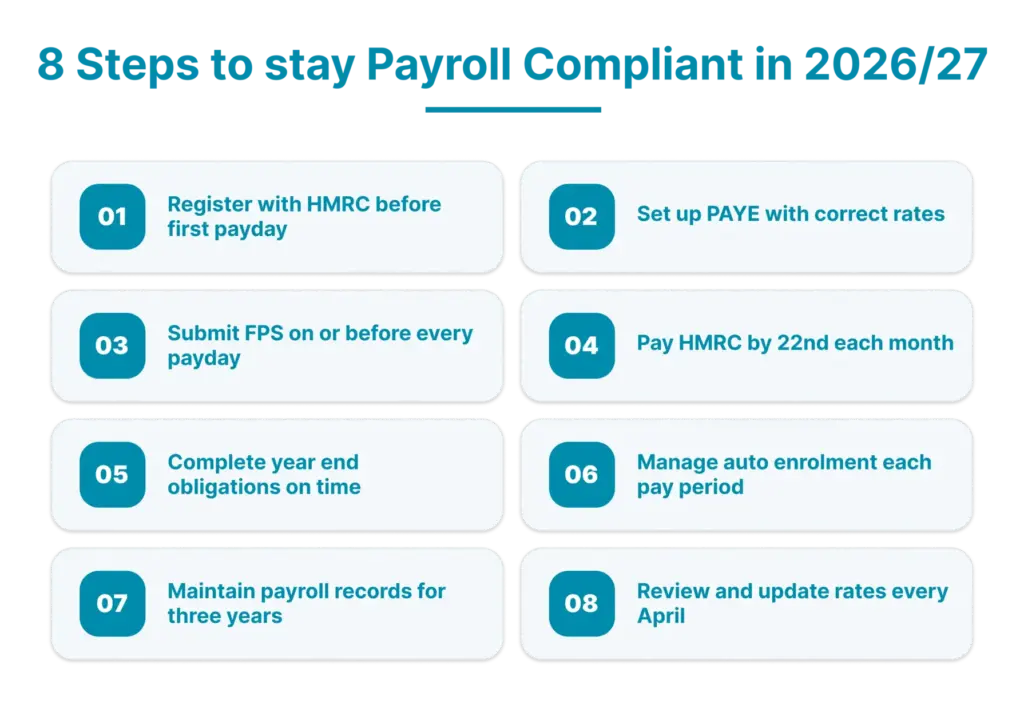

1. Register with HMRC

Register as an employer with HMRC before the first payday. Registration takes up to five working days and cannot be done more than two months before the first payroll date. HMRC issues an employer PAYE reference and an Accounts Office reference on registration both are required for all submissions and payments.

For every new starter, collect a P45 or complete the HMRC new starter checklist if no P45 is available. Right to work checks must be completed before employment begins. Records of those checks must be kept for two years after the employment ends.

Where the distinction between employee and contractor is not clear, use HMRC’s Check Employment Status for Tax (CEST) tool before making a decision. Misclassification shifts NIC and income tax liability back to the employer on discovery.

2. Set Up PAYE and apply the correct rates

Payroll software must calculate income tax, National Insurance, student loan deductions, and pension contributions accurately, and submit FPS and EPS reports directly to HMRC. The following rates are confirmed on GOV.UK and must be applied from the dates shown.

National Minimum and Living Wage from 1 April 2026:

| Worker category | Hourly rate |

|---|---|

| Aged 21 and over (National Living Wage) | £12.71 |

| Aged 18 to 20 | £10.85 |

| Aged under 18 (above school leaving age) | £8.00 |

| Apprentices under 19 or in first year of apprenticeship | £8.00 |

Salary sacrifice arrangements and unpaid working time can reduce effective hourly pay below the legal minimum. Both must be reviewed before assuming the rate has been met.

Statutory payment rates from 6 April 2026:

| Payment | 2026/27 rate |

|---|---|

| Statutory Sick Pay (SSP) | £123.25/week or 80% of average weekly earnings, whichever is lower |

| SMP, SPP, SAP, ShPP, SPBP, SNCP standard weekly rate | £194.32 or 90% of average weekly earnings, whichever is lower |

| SMP and SAP first 6 weeks | 90% of average weekly earnings |

Employer NIC is charged at 15% on earnings above £5,000 per year. The Class 1A NIC rate on benefits in kind is also 15%. The Lower Earnings Limit for qualifying for statutory family payments is £129 per week.

Student loan thresholds in 2026/27:

| Plan | Annual threshold |

|---|---|

| Plan 1 | £26,900 |

| Plan 2 | £29,385 |

| Plan 4 | £33,795 |

| Plan 5 | £25,000 |

Plan 5 is the default plan for new borrowers in England from April 2026. Starter checklists must be updated to reflect this.

Incorrect rates on even one pay run create discrepancies that take time to correct. Once rates are confirmed and software is configured, every payday carries its own set of reporting obligations.

3. Submit RTI Reports

The Full Payment Submission must be sent to HMRC on or before every payday, covering every employee paid in that period, including those earning below £96 per week.

Where statutory pay needs to be reclaimed, Employment Allowance claimed, or a nil payment month reported, an Employer Payment Summary must be submitted by the 19th of the following tax month.

RTI reporting informs HMRC what has been paid. The PAYE payment that follows must also reach HMRC within the correct deadline.

4. Pay HMRC on Time

PAYE and NIC for each tax month must reach HMRC by the 22nd electronically or the 19th by post. The tax month runs from the 6th to the 5th of the following month. Every payment must carry the correct 13-character Accounts Office reference. A payment made without it may not be allocated correctly and can produce a notice of arrears.

Employment Allowance of up to £10,500 is available to eligible employers in 2026/27, claimed through an EPS at the start of the tax year.

Monthly obligations repeat throughout the year. At the close of the tax year, a separate set of reporting deadlines must also be met.

5. Complete year-end obligations

After payroll has been run throughout the tax year, several submissions must be completed to close out the year with HMRC. Missing any of these deadlines results in financial penalties.

| Obligation | Deadline |

|---|---|

| Final FPS or EPS marked as year-end submission | 19 April |

| P60 issued to all employees in employment on 5 April | 31 May |

| P11D filed for expenses and benefits in kind | 6 July |

| P11D(b) employer declaration submitted | 6 July |

| Class 1A NIC payment on benefits | 19 July by post, 22 July electronically |

Employers registered to payroll benefits in kind before the start of the tax year do not file P11D forms for those benefits. Registration must be completed before 6 April and cannot be applied retrospectively.

Year-end reporting closes out the previous tax year. Pension obligations, however, run continuously and must be managed alongside every pay run throughout the year.

6. Manage Workplace Pension Auto-Enrolment

Every employer must assess their workforce each pay period and automatically enrol eligible employees. Eligible jobholders are those aged 22 to State Pension age earning over £10,000 per year.

Minimum contributions apply on qualifying earnings between £6,240 and £50,270 per year:

| Contribution | Minimum rate |

|---|---|

| Employer | 3% |

| Employee | 5% |

| Total | 8% |

Every three years, employers must re-enrol employees who previously opted out and now meet the eligibility criteria.

A re-declaration of compliance must be submitted to The Pensions Regulator within five months of the re-enrolment date.

7. Maintain proper payroll records

HMRC requires payroll records to be kept for a minimum of three years after the end of the relevant tax year. Records must include:

- Pay and deductions for each employee

- All FPS and EPS submissions made to HMRC

- Tax code notices received and applied

- Records of sick, maternity, paternity and holiday leave

Payroll data NI numbers, bank details, tax codes and salary figures is sensitive personal data under the UK GDPR and Data Protection Act 2018.

It must be stored securely and transferred only through protected channels. Inaccessible or missing records can result in an HMRC penalty of up to £3,000.

8. Review annually

At the start of each new tax year, rates, thresholds, and tax codes must be updated in payroll software before the first pay run. HMRC’s rates and thresholds page and the annual Employer Bulletin set out every change that applies from 6 April.

How to stay Payroll Compliant in the UK?

Payroll obligations recur on every payday, every month, and at year-end. These are the steps that keep a payroll process accurate throughout the year:

- Update payroll software at the start of every tax year. Rates, thresholds, and tax codes change on 6 April and must be applied before the first pay run

- Apply HMRC coding notices as soon as they are received. Deferring them creates errors across multiple pay runs

- Set reminders for every recurring deadline: FPS on payday, PAYE by the 22nd, EPS by the 19th, P60 by 31 May, P11D by 6 July

- Reconcile the HMRC PAYE online account each month to confirm submitted figures match what HMRC shows as owed

- Review employee records at least once a year. NI numbers, tax codes, student loan plans, pension enrolment status, and right to work documents all need to be current

- Register to payroll benefits in kind before 6 April 2027. Mandatory payrolling of all taxable benefits takes effect from April 2027 and registration must be completed before the new tax year begins

What changed in 2026/27?

The 2026/27 tax year has introduced several changes that affect payroll costs and processes for most UK employers.

- SSP payable from day one of absence from 6 April 2026; the three waiting days and the Lower Earnings Limit have been removed; rate is £123.25 per week

- Employer NIC threshold reduced from £9,100 to £5,000 per year from 6 April 2026, increasing employer NIC costs at every pay level

- Paternity leave became a day-one employment right from 6 April 2026, removing the 26-week continuous service requirement for taking leave. The 26-week service requirement still applies for Statutory Paternity Pay (SPP) eligibility.

- Student Loan Plan 5 default plan for new borrowers in England from April 2026; starter checklists must be updated

- Mandatory payrolling of benefits from April 2027, all taxable benefits must be processed through payroll in real time; P11D forms will no longer apply; employers must register with HMRC before 6 April 2027

Conclusion

The 2026/27 tax year has added to the scope and cost of payroll compliance for UK employers. Lower NIC thresholds revised statutory rates, new employment rights, and the shift to mandatory benefits payrolling from April 2027 all require attention across the year.

This checklist covers every obligation in the order it arises, so each area can be confirmed and any gaps addressed before they become penalties.

DNS CloudCo provides a full payroll service for UK businesses, covering PAYE calculations, pension contributions, P60 and P11D filings, and year-end reporting. Our payroll team manages every HMRC deadline on your behalf. To find out how we can support your business, call: 01908 886755, email: info@dnscloudco.co.uk .

FAQs

What are the payroll deadlines UK employers must not miss?

FPS must be submitted on or before every payday. PAYE and NIC must reach HMRC by the 22nd of each month electronically. P60s are due by 31 May and P11D forms by 6 July.

What is the employer NIC rate and threshold for 2026/27?

Employer NIC is charged at 15% on employee earnings above the secondary threshold of £5,000 per year. This threshold reduced from £9,100 in 2025/26, increasing the NIC cost for most employers across all pay levels.

What is Employment Allowance and who can claim it?

Employment Allowance allows eligible employers to reduce their annual employer NIC bill by up to £10,500. It is claimed through an EPS submission at the start of the tax year.

What is the SSP rate for 2026/27 and when is it payable?

SSP is £123.25 per week or 80% of average weekly earnings, whichever is lower. From 6 April 2026, it is expected to be payable from the first day of absence (subject to final legislative implementation). The three waiting days and the Lower Earnings Limit have both been removed.

When must P60s be issued to employees?

P60s must be given to all employees in employment on 5 April by 31 May. They can be issued electronically where the employee has agreed to receive them in that format.

Do I need to file a P11D if I payroll my benefits?

No, where you have registered with HMRC to payroll benefits in kind before the start of the tax year, P11D forms are not required for those benefits. Tax is deducted through the employee’s pay in real time instead.

What payroll records must I keep and for how long?

Pay & Deductions, HMRC submissions, tax code notices and leave records must be kept for at least three years after the end of the relevant tax year. Right to work documents must be kept for two years after the employment ends.

What is re-enrolment and when does it apply?

Re-enrolment requires employers to reassess and re-enrol employees who previously opted out of the workplace pension and now meet the eligibility criteria. It must be carried out every three years and followed by a re-declaration of compliance to The Pensions Regulator within five months.

When does mandatory payrolling of benefits take effect?

From April 2027, all taxable benefits must be processed through payroll in real time and P11D forms will no longer apply. Employers not already payrolling benefits must register with HMRC before 6 April 2027. Registration cannot be applied mid-year.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.