When a business buys equipment, a van or machinery, the accountant records depreciation in the profit and loss account. HMRC does not accept that depreciation as a tax deduction. Instead, HMRC operates its own separate system called capital allowances, which determines how much of an asset’s cost can be deducted from taxable profits and in which year. A business that claims correctly can write off up to £1 million of qualifying expenditure in the same year it buys the asset. One that does not claim or claims the wrong allowance, waits years for the same relief.

2026 brings three specific changes every UK business should know about.

The main rate writing down allowance (WDA) drops from 18% to 14% from 1 April 2026 for companies and 6 April 2026 for sole traders and partnerships. A new 40% first-year allowance (FYA) applies to qualifying expenditure from January 2026. And the 100% FYA for zero-emission cars has been extended to April 2027. For businesses with existing pool balances or accounting year-ends that spans April 2026, these changes need careful attention.

Key Takeaways

- Limited companies can claim Full Expensing on qualifying new plant and machinery with no upper monetary limit but this relief is not available to sole traders or partnerships, which is a planning point many business owners miss.

- The new 40% FYA introduced from 1 January 2026 is the first front-loaded relief that sole traders, partnerships and leasing businesses can access on top of the AIA filling a gap that has existed since Full Expensing launched in 2023.

- Integral features such as heating systems, electrical systems and air conditioning within a commercial building fall into the special rate pool at 6% WDA if the AIA is not used which is why directing AIA to these assets tends to be more tax-efficient than using it on standard plant.

- Businesses with an accounting year that spans April 2026 will face a hybrid WDA rate rather than a clean 14% the exact rate depends on how many days fall before and after the change date.

What are Capital Allowances?

Capital allowances are a form of tax relief that lets UK businesses deduct the cost of capital assets from their taxable profits.

They exist because HMRC does not allow accounting depreciation the charge businesses make in their accounts for the gradual reduction in value of assets, which is not allowed as a tax deduction.

Instead, HMRC uses its own system, a set of rules that determine how much of an asset’s cost can be deducted from profits and when.

What can you claim on?

The main category is plant and machinery. It includes:

- Equipment and machinery: computers, office furniture, manufacturing tools

- Commercial vehicles: vans, lorries and trucks (not cars, which follow separate rules)

- Fixtures that are physically built into a commercial property, such as heating systems, electrical systems, air conditioning, lifts and hot and cold water systems HMRC classifies these as integral features

- Solar panels and other renewable energy installations

- IT systems and technology

You can also claim the Structures and Buildings Allowance (SBA) at 3% per year on qualifying construction costs for new non-residential commercial buildings and structures, as well as separate allowances for research and development and patent rights.

You cannot claim this tax relief on land, residential property (with limited exceptions for communal areas in some multi-unit buildings) or items bought purely for resale.

Capital vs Revenue Expenditure

Capital expenditure refers to money spent on buying or improving long-term assets such as machinery, vehicles, equipment, or buildings. These assets are expected to benefit the business over several years and are not used up within a single accounting period.

Revenue expenditure covers the regular operating costs needed to run the business on a daily basis. This includes expenses like wages, rent, utilities, repairs and consumables that are fully used within the same financial year.

The main difference is in how they are treated in accounts. Capital expenditure is not written off immediately and may qualify for capital allowances over time. Revenue expenditure is deducted directly from business profits in the same accounting period.

The Main Types of Capital Allowances in 2026

Each allowance works differently, applies to different types of expenditure and is available to different types of business. Using the right one in the right order is what determines how much tax relief you actually get and how quickly.

| Allowance | Rate | Applies To | Business Type |

|---|---|---|---|

| Annual Investment Allowance (AIA) | 100% up to £1,000,000/year | Most plant and machinery (not cars) | All businesses |

| Full Expensing | 100%, no cap | New qualifying main rate P&M | Companies only |

| Full Expensing 50% FYA | 50%, no cap | New qualifying special rate P&M | Companies only |

| New 40% FYA (from Jan 2026) | 40% in year one | New unused main rate P&M | Companies and unincorporated |

| WDA main pool | 14% per year (from April 2026) | General P&M not covered above | All businesses |

| WDA special rate pool | 6% per year | Integral features, long-life assets, high-emission cars | All businesses |

| 100% FYA zero-emission cars | 100% in year one (to April 2027) | New zero-emission cars | All businesses |

| Structures and Buildings Allowance | 3% per year (straight-line) | New qualifying commercial structures | All businesses |

Note: Full Expensing and the 50% FYA are available to limited companies only, sole traders and partnerships cannot claim these reliefs.

- The new 40% FYA includes assets purchased for leasing within the UK unlike Full Expensing, which specifically excludes leasing.

- Cars are excluded from AIA across all allowance types, separate rules apply based on CO₂ emissions.

The most important planning principle for most businesses is this: use AIA first and direct it towards your most expensive qualifying assets especially integral features, which would otherwise only attract 6% WDA.

For companies, Full Expensing covers anything above the AIA limit at 100% with no cap.

The super deduction which gave companies 130% relief on qualifying plant and machinery ended on 31 March 2023 and was replaced by Full Expensing.

Leaving assets to accumulate in the main pool at 14% WDA is the slowest route to relief and should generally be the last resort.

Three Key Tax Relief Changes in 2026 to plan for

Three changes took effect in 2026 that affect how businesses structure capital expenditure. Each one is distinct and understanding how they interact matters particularly for businesses with year-ends that do not align neatly with the April change dates.

1. Main rate WDA reduces from 18% to 14%

The main rate WDA reduces from 18% to 14% from 1 April 2026 for companies and 6 April 2026 for sole traders and partnerships. The special rate pool stays at 6%.

Businesses with accounting periods spanning these dates use a hybrid rate, apportioned by days before and after the change. A company with a 31 December 2026 year-end has 90 days at 18% and 275 days at 14%, giving a blended rate of approximately 14.99%.

Businesses claiming AIA or Full Expensing on all expenditure will be largely unaffected. Those with historic pool balances or assets outside AIA and Full Expensing will simply receive relief more slowly than before.

2. New 40% first-year allowance from 1 January 2026

A new 40% FYA applies to expenditure on new and unused main rate plant and machinery from 1 January 2026.

It also covers assets bought for leasing within the UK an area Full Expensing specifically excludes. Cars and second-hand assets do not qualify.

For most SMEs spending below the £1 million AIA limit, this FYA rarely comes into play. For larger capital spenders and unincorporated businesses above the AIA cap, it provides useful front-loaded relief in the year of purchase.

3. Zero-emission car 100% FYA extended to April 2027

The 100% FYA for brand-new zero-emission cars and electric vehicle charging points has been extended by one year to 31 March 2027 for companies and 5 April 2027 for income tax businesses.

New or used non-electric cars with CO₂ of 1–50g/km use the 14% main rate WDA. Cars above 50g/km go into the special rate pool at 6%.

How Tax Relief works for Cars, Vans, Integral Features and Solar Panels?

Not every asset follows the same rules and getting the classification wrong is one of the most frequent and expensive errors businesses make. Here is how the main asset types are treated.

Vans and Commercial Vehicles

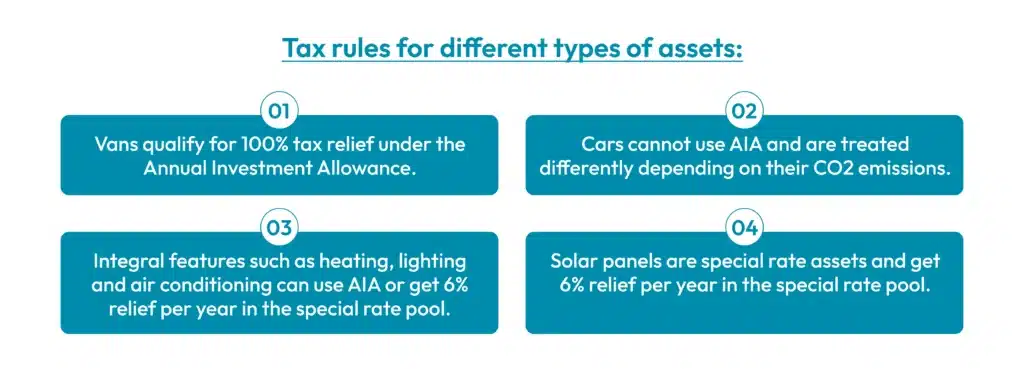

Vans, lorries and trucks qualify for the Annual Investment Allowance at 100%, giving full tax relief in the year of purchase. A sole trader who uses a van partly for private journeys must reduce the claim to reflect only the business-use proportion.

A limited company can claim capital allowances on the full cost of a van. If an employee uses the van for private journeys beyond incidental use, a flat-rate van benefit in kind charge applies, this is separate from the capital allowances claim and does not reduce it.

Cars

Cars cannot use the AIA. New zero-emission cars attract a 100% FYA until April 2027. Cars with CO₂ emissions of 1–50g/km go into the main rate pool at 14% WDA. Cars above 50g/km go into the special rate pool at 6% WDA.

Integral Features

Heating systems, electrical systems, air conditioning, lifts and hot and cold-water systems built into a commercial property are treated as integral features under the Capital Allowances Act 2001.

They qualify for AIA at 100%, but if AIA is not claimed, they fall into the special rate pool at 6% WDA. The practical implication is clear: use AIA on integral features before directing it to assets that would otherwise sit in the faster-moving main pool.

Solar Panels

Solar panels and other renewable energy installations qualify as plant and machinery but fall into the special rate pool at 6% WDA unless AIA is used. Given how slowly relief accumulates at 6%, claiming AIA on solar panels is generally the better approach wherever the annual limit allows for it.

Capital Allowances for Startups and Self-Employed Businesses

Many new business owners and sole traders pay more tax than necessary on capital purchases not because the rules are unfair, but because they are not aware of how the system actually works.

New Businesses

A startup can claim capital allowances from its very first accounting period. There is no minimum trading period required. A business incorporating in 2026 and spending £50,000 on equipment in year one can claim 100% of that cost via AIA, directly reducing the corporation tax bill from the outset.

Sole traders and Partnerships

Self-employed individuals and partnerships can claim AIA and the new 40% FYA, but not Full Expensing, which is restricted to companies. Sole traders and partnerships claim through the self-assessment tax return using the SA103 (self-employment) pages.

Limited companies claim through the CT600 corporation tax return. Where an asset is also used for personal purposes, only the business-use proportion qualifies.

Depreciation in Accounts vs Capital Allowances

These are two separate calculations and one does not replace the other. The depreciation a business records in its accounts has no effect on the tax bill, as HMRC does not allow it as a deduction. Instead, it applies its own system to determine how much of the asset cost can be claimed.

A new business that only records depreciation and does not claim this relief will often overpay tax, especially in the first year when capital spending is typically higher.

Conclusion

Capital allowances are one of the UK’s most valuable business tax reliefs, yet under-claiming is widespread especially among sole traders and new businesses unaware that accounting depreciation and tax relief are calculated separately.

The 2026 changes add real complexity. The WDA reduction, hybrid rates for straddling year-ends and the new 40% FYA alongside AIA and Full Expensing mean the most tax-efficient approach depends on your business structure, asset type and accounting year-end.

Getting this right is the difference between claiming relief in year one and waiting years for it to filter through.

DNS CloudCo’s chartered accountants work with UK limited companies, sole traders and startups to ensure these allowances are claimed in full and structured correctly. Book a consultation today.

Frequently Asked Questions

What are capital allowances in the UK?

A tax relief that lets businesses deduct the cost of qualifying assets from taxable profits, instead of using accounting depreciation which HMRC does not accept for tax purposes.

What is the Annual Investment Allowance limit for 2026–27?

The AIA limit is £1,000,000 per year. It allows 100% tax relief on most plant and machinery purchases, excluding cars, for all business types.

What is Full Expensing and who can claim it?

Full Expensing allows 100% relief on new qualifying plant and machinery with no cap. It is only available to UK limited companies, not sole traders or partnerships.

What happens when I sell an asset I have claimed capital allowances on?

The sale proceeds are added back into the pool or deducted from the claim. This may create a balancing charge or allowance, adjusting your taxable profits accordingly.

What is the difference between capital expenditure and revenue expenditure?

Capital expenditure is for long-term assets like equipment or vehicles. Revenue expenditure covers day-to-day costs like rent or wages and is deducted immediately from profits.

What happened to the super deduction?

The super deduction ended on 31 March 2023. It was replaced by Full Expensing, which provides 100% relief on qualifying new plant and machinery for companies.

What is the writing down allowance and how does it work?

Writing down allowance spreads tax relief over time. Assets are grouped into pools and deducted annually at set rates, 14% for main pool and 6% for special rate pool.

What capital allowances can I claim on a van?

Vans qualify for 100% relief under AIA. Sole traders must adjust for personal use, while companies can claim full cost, with private use treated separately for tax purposes.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.