When starting a business in the UK, one of the first things to decide is whether to work as self-employed or set up a limited company. Many people start as self-employed because it is easier to set up and manage in the early stages.

This choice is not just about registration. It can affect how much tax is paid, how much personal risk is involved, and how much day-to-day paperwork is needed.

Understanding the difference between being self-employed and running a limited company can make it easier to choose what works best for your business.

Key Takeaways:

- Self-employed and limited company are taxed in different ways

- A Limited company mainly helps with protecting personal assets, not just tax

- The right setup depends on three things: income, risk, and what clients expect

- Switching from self-employed to a limited company is simple, but timing is important

The Legal Difference Between Self-Employed and a Limited Company

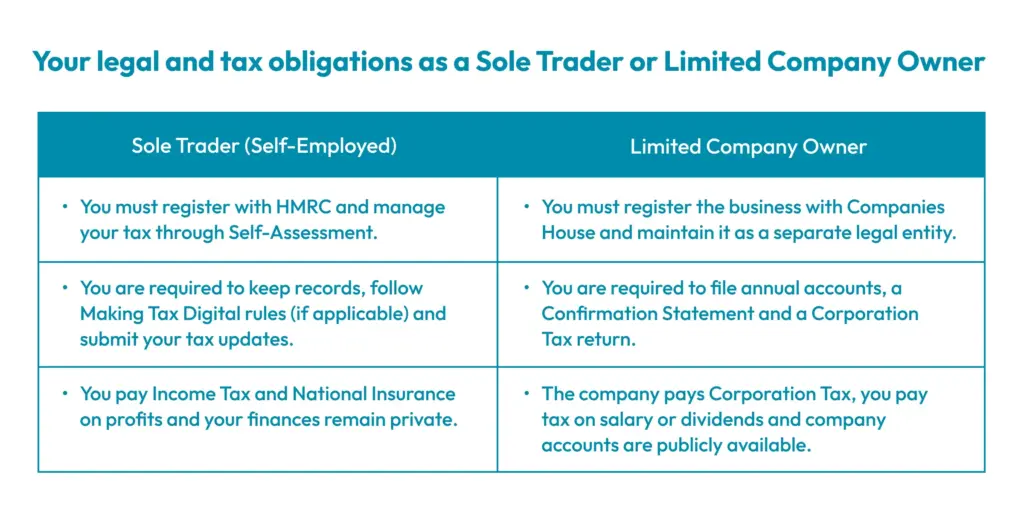

The main difference between being self-employed and running a limited company is that a limited company is separate from the person who owns it.

If you are self-employed, there is no legal difference between you and the business. Any money the business makes belongs to you, but you are also responsible for any debts or problems linked to the business.

A limited company works in a different way. The business and the owner are treated separately. The company can make money, sign agreements and deal with debts in its own name. You still manage the business as the director, but your personal money is usually separate from the company.

This can help if the business runs into financial or legal problems. In most cases, your personal assets are more protected compared to being self-employed.

Main differences between both structures:

A sole trader keeps the profits after paying tax and is personally responsible for business debts.

A limited company pays Corporation Tax on profits, and directors usually take income through salary and dividends.

A sole trader’s financial information stays private, while limited companies must file some details with Companies House.

How is each structure taxed?

Tax is often where the difference between sole trader and limited company status becomes most noticeable. Sole traders pay tax directly on business profits, while limited company directors usually receive income through a combination of salary and dividends.

| Tax & Structure Factor | Self-Employed Sole Trader | Limited Company Director |

|---|---|---|

| Tax on profits | Income Tax on business profits through Self-Assessment | The company pays Corporation Tax: 19% on profits up to £50,000, 25% on profits above £250,000, with marginal relief available in between |

| Income tax rates | 20%, 40%, or 45%, depending on total taxable income | Salary is taxed under normal Income Tax bands. Dividends above the £500 dividend allowance are taxed separately |

| Dividend tax rates | Not applicable | 10.75% (basic rate), 35.75% (higher rate), and 39.35% (additional rate) |

| National Insurance | Class 4 National Insurance at 6% on profits between £12,570 and £50,270, then 2% above £50,270 | The company may pay Employer’s National Insurance at 15% on salary above the applicable threshold. Directors may also pay Employee National Insurance on salary. No National Insurance is charged on dividends |

| Personal Allowance | £12,570, meaning no Income Tax below this threshold | £12,570, which can usually be used against the director’s salary |

| Tax return requirements | One annual Self-Assessment tax return | The company files annual accounts and a Corporation Tax return, and the director may also need a personal Self-Assessment return |

One thing that can matter when starting a business is how losses are treated.

If a sole trader makes a loss in the first year, that loss can sometimes be set against other taxable income from the same year. This may reduce an existing tax bill or lead to a refund from HM Revenue & Customs.

A limited company treats losses differently. In most cases, the loss stays within the company and is carried forward to reduce Corporation Tax on future profits. It usually cannot be used for immediate personal tax relief.

The profit point where the calculation changes

A limited company becomes worth considering once annual profit reaches around £30,000. Below this, the tax saving is too small to cover the extra costs of running a company.

Above £50,000, the saving becomes clear. Dividends are taxed at 10.75%, which is significantly lower than the combined Income Tax and National Insurance a sole trader pays on the same profit.

| Profit Level | Suggested Structure | Reason |

|---|---|---|

| Under £30,000 | Self-employed | Lower running costs and simpler administration |

| £30,000 to £50,000 | Consider a limited company | Tax savings may begin to justify the extra responsibilities |

| Above £50,000 | Limited company | More flexibility in how income is taken |

It is also important to factor in accountancy fees. A limited company usually costs more to manage than a sole trader business. The right decision depends on the overall financial benefit after those extra costs are included.

How will Making Tax Digital affect Sole Traders?

From April 2026, some sole traders will have to follow new HMRC reporting rules.

If your self-employed income is more than £50,000, you will need to keep digital records and send updates to HMRC every three months using approved software. At the moment, most sole traders only submit one Self Assessment tax return each year.

The same rules are expected to apply from April 2027 for people earning between £30,000 and £50,000.

Limited companies are not part of these changes. They follow different tax reporting rules.

The role of Limited Liability in business structure decisions

Tax receives attention, but liability protection is frequently the more significant factor in any limited company vs self-employed decision.

As a sole trader, there is no legal boundary between you and your business. If a client raises a claim or a supplier is owed money the business cannot repay, that claim is against you personally. Your savings, your vehicle and in serious cases your home are all reachable.

A limited company limits that exposure. Creditors can only pursue company assets unless fraud, wrongful trading, or a personal guarantee is involved.

When liability protection matters most?

- Your work carries financial or legal risk – consulting, construction, IT, financial services

- Your contracts involve significant sums of money

- You are taking on employees or subcontractors

- The business holds equipment or stock of meaningful value

For lower-risk work, unlimited liability is often an acceptable position. Where a single claim could cause serious personal financial difficulty, incorporating is a risk management decision first and a tax decision second.

Administration, privacy and how clients see you?

Both structures carry different day-to-day responsibilities. The level of financial visibility and administrative burden also differs significantly depending on which structure you choose.

In certain sectors, especially financial services or larger corporate procurement environments, operating as a limited company is expected. In these situations, the self-employed or limited company question may already be answered by client requirements.

Which structure is right for you?

Choosing between self-employed and limited company depends on your income, risk level, client requirements, and future plans. These four questions help guide the decision.

What are your annual profits?

Below £30,000, self-employed is usually the more practical choice. Above £35,000, a limited company typically produces a better net outcome once fees are factored in.

What is your risk exposure?

If a business debt or client claim could create serious difficulty for your personal finances, the cost of incorporating is justified by the protection it provides separate from any tax benefit.

What do your clients expect?

Some clients will only contract with a limited company. Check what your market actually requires before making the decision.

Are you planning to grow?

If you intend to take on staff, bring in investment, or sell the business at a later point, a limited company gives you the right legal framework to do so. A sole trader structure does not.

These factors determine whether self-employed vs limited company status aligns with long-term objectives.

Moving from Self-Employed to a Limited Company

Starting as self-employed and incorporating later is a practical approach many business owners take. Once profits reach the crossover point or a key client requires it the move makes sense.

The process involves registering at Companies House, notifying HMRC, opening a business bank account in the company name, updating contracts and transferring any business assets across.

An accountant should review the timing before you make the switch. The point in the tax year at which you incorporate can affect your position in that first year of trading as a company.

Conclusion

The right structure depends on your income, the level of risk in your work and your future plans.

For smaller and simpler businesses, staying self-employed is often easier to manage. If profits increase or the business starts growing, a limited company may become a better option.

If you are unsure which setup is right for you, it is best to speak with an accountant before making a decision.

DNS Cloud Co helps sole traders and limited companies across the UK with business setup and accounting support.

Frequently Asked Questions

What is the difference between self-employed and a limited company?

A self-employed person and the business are the same thing, any profit is treated as personal income, a limited company is separate, the company earns the money and pays Corporation Tax, the owner usually takes money through salary and dividends.

Is it better to be self-employed or a limited company?

Self-employed is easier to manage and has less paperwork, a limited company can work better when income is higher or when there is a need for more separation between personal and business finances.

What is the difference between self-employed and a company director?

A self-employed person reports business profit as personal income, a company director earns through salary and dividends, the company itself is taxed on profits before anything is paid out.

Can I switch from self-employed to a limited company later?

Yes, many people start as self-employed and move to a limited company later, it involves setting up the company, registering it, and moving the business into it.

Do limited company directors pay National Insurance?

Yes, on salary only, dividends are not subject to National Insurance.

When should I think about changing status?

When profits increase, work becomes more regular, or there is a need for more separation between personal and business finances.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.