Running a business as a sole trader works well in the early stages. As profits increase, many business owners ask whether a limited company is worth considering.

The structure has real advantages, but the added responsibilities are worth understanding before making the switch. This guide covers both.

Key Takeaways

A limited company is a separate legal entity, so your personal assets are not at risk if the business has debts

Directors can draw income through salary and dividends, which is often more tax efficient than income tax on all earnings

A limited company requires annual accounts, confirmation statements and corporation tax returns every year

Company finances are on public record at Companies House, unlike sole trader finances which remain private

The structure generally makes financial sense when profits reach around £30,000 or more or for contractors working outside IR35

Note : This article was updated and republished on 01 May 2026 to include the latest information on UK limited company structures, corporation tax rates, Companies House filing requirements and key advantages and disadvantages relevant to business owners considering incorporation.

The Advantages of a Limited Company

Many businesses consider incorporation once operations grow or profits increase. A limited company structure offers several benefits.

Limited Liability Protection

One of the most important advantages of limited company ownership is limited liability.

- A company operates as a separate legal entity under the Companies Act 2006

- Shareholders are usually responsible only for the value of their shares

- Personal assets are generally protected if the company cannot meet its obligations

Tax Efficiency Through Corporation Tax and Dividends

Tax planning is one of the main reasons business owners consider switching to a limited company.

- Companies pay corporation tax on profits

- Rates range between 19% and 25% according to HM Revenue and Customs

- Directors may take income through a mix of salary and dividends

Improved Business Credibility

Operating through a company can strengthen professional reputation.

- Businesses registered with Companies House often appear more established

- Larger organisations may prefer working with incorporated suppliers

- A company structure can increase trust with clients and partners

Easier Access to Investment

Limited companies are generally better positioned to raise funding.

- Companies can issue shares to investors

- Ownership can be divided among multiple shareholders

- This structure supports long term business expansion

Business Continuity

A limited company can continue operating even if ownership changes.

- Shares can be transferred to new owners

- The business structure remains separate from the founder

- Operations can continue despite ownership transitions

The Disadvantages of a Limited Company

While the benefits are significant, the disadvantages of limited company ownership should also be considered.

Increased Administrative Responsibilities

Running a company requires more reporting and documentation.

- Directors must file annual accounts with Companies House

- Companies must submit a confirmation statement each year

- Corporation tax returns must be filed with HM Revenue and Customs

Reduced Financial Privacy

Certain company information becomes publicly available.

- Company accounts can be viewed on the Companies House register

- Director details appear on the public company record

- Business information becomes accessible to competitors or clients

Higher Professional Costs

Compliance obligations often increase support costs.

- Many companies require professional help with annual accounts

- Corporation tax reporting may require specialist advice

- Payroll and dividend planning can add administrative expense

Restrictions on Accessing Profits

Profit withdrawals operate differently in a company.

- Sole traders can withdraw profits directly from business income

- Directors must take money through salary or dividends

- Dividends can only be paid from profits after corporation tax

IR35 Considerations for Contractors

Contractors using companies must consider IR35 legislation.

- IR35 determines whether a contractor is treated as an employee for tax purposes

- Contracts inside IR35 may remove certain tax advantages

- Some clients assess IR35 status before engaging contractors

Limited Company vs Sole Trader: Tax Comparison

The differences become much clearer when you put the two structures side by side.

| Factor | Sole Trader | Limited Company |

|---|---|---|

| Income tax | 20%, 40%, 45% on profits | Corporation tax roughly 19%–25% |

| National Insurance | Class 2 and Class 4 NICs | Often lower through salary and dividends |

| Administration | Annual self-assessment | Companies House filings and corporation tax |

| Liability | Unlimited | Limited to share value |

| Privacy | Private | Accounts publicly available |

This comparison highlights the practical advantages and disadvantages of a limited company.

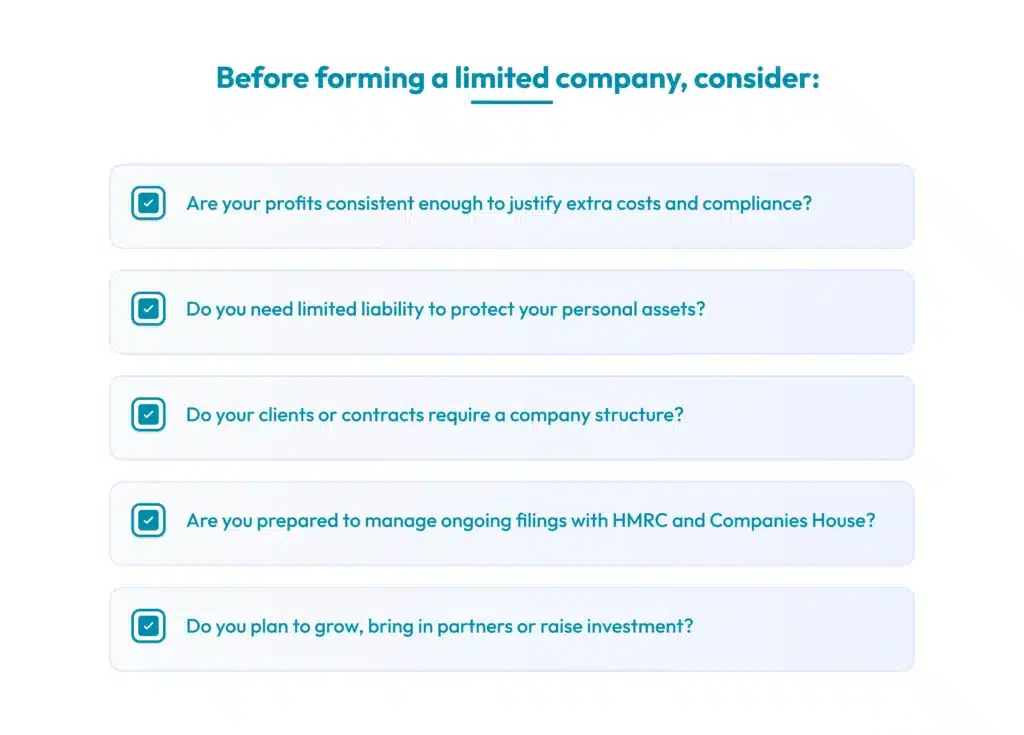

Who should consider forming a Limited Company?

A limited company may suit:

- Sole traders earning around £30,000 to £35,000 or more in profit

- Contractors working outside IR35 rules

- Startup founders planning to raise investment

- Business owners seeking stronger limited liability protection

However, it may be less suitable for very small businesses or those who prefer simpler administration.

Answering these questions can help business owners decide whether a limited company structure aligns with their goals.

Conclusion

Not every business needs a limited company. For some it makes clear financial sense, for others the extra admin and costs outweigh the benefits, at least at their current stage.

If you want professional advice on whether incorporating is right for you, contact DNS CloudCo on 01908 886755 or email info@dnscloudco.co.uk

FAQs

What are the main advantages of a limited company in the UK?

The main advantages are that your personal assets are protected from business debts, you can pay yourself through salary and dividends which is more tax efficient and clients tend to take limited companies more seriously.

What are the disadvantages of forming a limited company?

You have more paperwork to deal with, you need to file accounts and a confirmation statement with Companies House every year, accountancy cost go up and you cannot just take money out whenever you want.

What are the Companies House filing requirements for a limited company?

You need to file your annual accounts, send a confirmation statement once a year and make sure your company details on the register are always up to date.

How does limited liability protection work?

The company is legally separate from you, so if the business cannot pay what it owes, your personal money and assets are not touched.

What is the difference between corporation tax and income tax?

The company pays corporation tax on what it earns, you pay income tax on your salary and dividend tax on dividends and dividends are taxed at a lower rate.

Can I convert from sole trader to limited company?

Yes, you register the company with Companies House, set up a business bank account and shift your work across to the new structure.

Does forming a limited company affect National Insurance?

Most directors take a small salary and add dividends on top and because dividends do not have National Insurance on them, you usually end up paying less than a sole trader would.

What is IR35?

IR35 looks at whether a contractor should really be taxed like an employee and if your contract falls inside it, most of the tax benefits of having a limited company go away.

Should I form a limited company if I earn over £30,000?

It is worth looking into at that level, but your expenses, how you take income and your tax situation all affect whether it is the right move, so speaking to an accountant first makes sense.

Divyanshi is a subject matter expert in the UK accounting space, creating clear and easy-to-read content for accountants and businesses. She covers topics such as VAT returns, Self-assessment tax, bookkeeping, business planning and Year-end accounts. By understanding the common challenges faced by accountants and business owners, she focuses on writing content that answers real questions and simplifies complex topics. Her approach keeps information clear, relevant and useful for everyday business needs.